Buses, bandits, and the broken banks that created fintechs

Before apps and APIs, there was fear, failure, and a few bold bets on technology.

Notadeepdive is brought to you by Credit Direct. Download the app here.

If you missed Sunday’s Notadeepdive, catch up here.

Two weeks ago, I wrote about Jumia’s $13.7 million cloud bill and how the e-commerce giant is responding to competition from Chinese players Temu and Shein.

Adedeji Olowe shared an interesting response:

“If Shein and Temu are making a killing (I have used them to buy rubbish too), maybe our operators have been wrong about the African market. All this talk about limited spend or market immaturity might just be bad execution hiding behind excuses.

With Jumia Food, they left food on the table. Chowdeck just came, picked it up, and ate it properly.

So maybe the problem isn’t the market. Or is it Jumia? They throw money at problems but can’t execute. Every vertical they struggle with ends up being dominated by someone else who just builds and ships better.

Feels like their entire playbook is to show up early, spend big, and fumble the basics. Then when someone comes in with focus and discipline, they lose the market they were supposed to own.

The question isn’t whether the African market is ready. It’s whether the operator is.”

TOGETHER WITH CREDIT DIRECT

With Credit Direct Checkout, you can access up to ₦1,000,000 in credit to shop now and pay later. Start by checking how much you qualify for.

For this week’s Notadeepdive, I’ll share an idea I’ve been working on for a few weeks. Let me know what you think. Let’s get into it:

Buses, Bandits, and the Broken Banks that Created Fintech

On September 5, 2003, a luxury bus traveling from Abuja to Lagos was ambushed by armed robbers. On board were police officers, hired by the passengers at a time when attacking long-distance buses had become a thriving criminal enterprise.

That night, the armed policemen changed nothing. Four passengers were killed, and ₦3.5 million disappeared into the darkness.

Despite these incidents, moving cash remained popular, not because people loved the risk, but because the banks hadn’t earned their trust.

It’s easy to forget how fragile Nigeria’s financial system was from the early 80s to the early 2000s. Commercial banks routinely collapsed under the weight of bad loans, currency arbitrage schemes, and cooked books. And in that climate of institutional distrust, financial technology wasn’t impressing the public.

Some banks tried nonetheless.

In 1990, Societe Generale installed Nigeria’s first working ATM branded CashPoint 24. Second to the ATM race was First Bank, which installed “First Cash,” a nationwide ATM system in 1991.

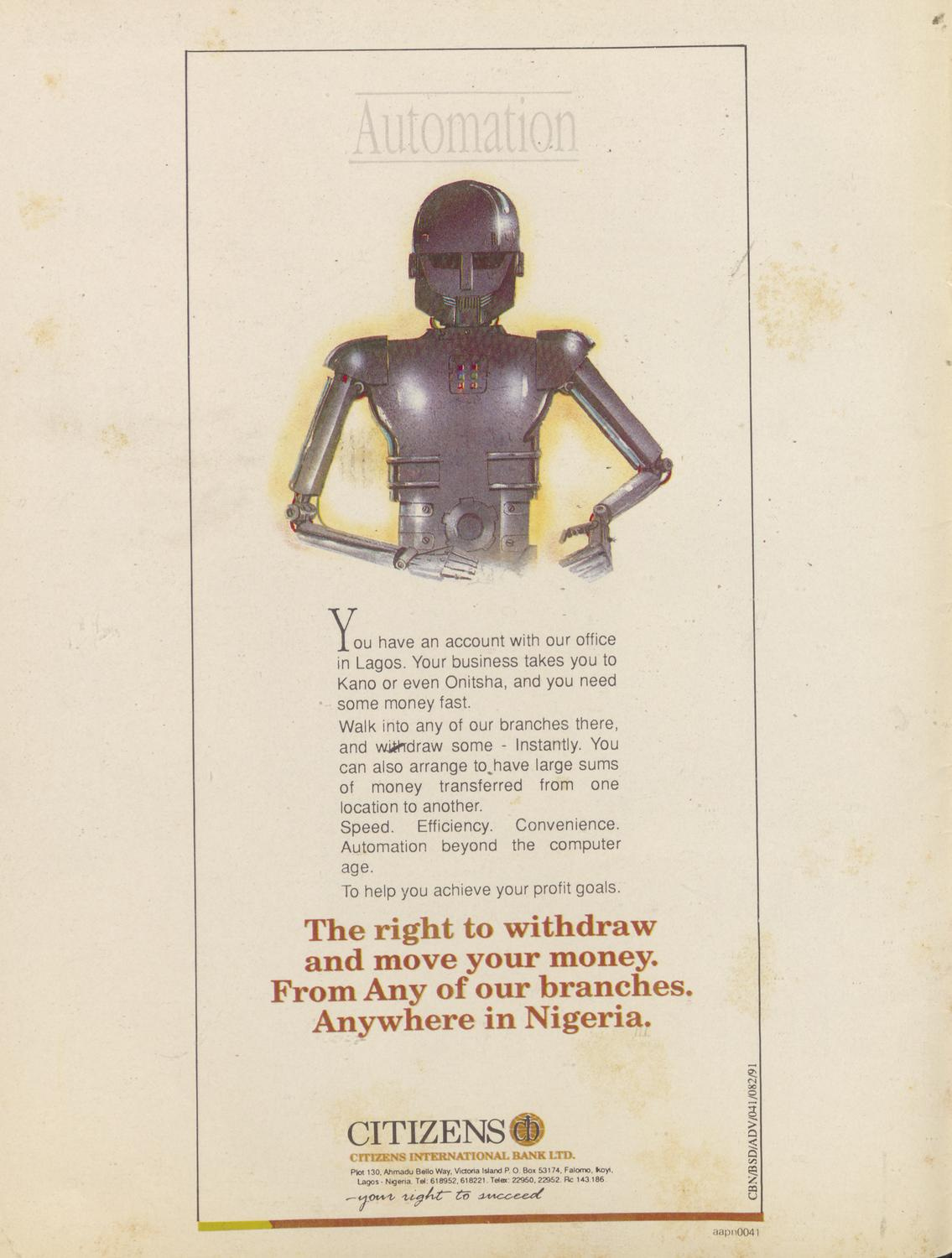

Citizen Bank also advertised a new kind of convenience: customers could walk into any branch to withdraw or transfer large sums. These were early bets that technology could be a competitive edge in a crowded field.

According to Seth Apati’s The Nigerian Banking Sector Reforms, the number of licensed banks in Nigeria grew from 40 in 1985 to 107 by 1990. In that chaotic field, differentiation was everything.

But banking wasn't booming because of better customer service or smart technology. The catalyst was the creation of the Second-Tier Foreign Exchange Market (SFEM) in 1986. The STFEM created a parallel market and an opportunity for banks to profit by buying foreign currency at official rates and selling it on the black market (just like the Emefiele years).

“The gap between the official rate and the parallel or black market rates meant that banks, in an era of porous monitoring, could make economic rent by arbitraging foreign currency between the two markets and earn an undisclosed parallel market premium,” Apati wrote.

These FX gains were lucrative but blinding. Who needed interoperability or reliable ATMs when arbitrage could fatten the balance sheet?

But the good times didn’t last.

As regulatory scrutiny of FX dealings increased, the cracks became impossible to hide. Many banks had been ignoring basic lending rules. Some cooked their books. Others were little more than fronts for looting depositors’ funds.

In 1994, Kapital Merchant Bank, United Commercial Bank, and Financial Merchant Bank were liquidated. Another bank had its licence suspended. By 1995, the Central Bank had taken over 13 distressed banks and placed dozens more under “holding actions” through the NDIC (Brownbridge,1998).

By 1998, the rot had reached critical mass. That year, CBN Governor Paul Ogwuma revoked the licences of more failed banks, citing ₦19 billion in trapped depositor funds. The wave of collapses continued into the next decade. According to Bright Njoku, 12 more banks failed between 2000 and 2006, bringing the total to 45.

Banks owned by former governors and the country’s elite went under, with no consequence or penalty, and “wonder banks,” a term synonymous with heartbreak, entered the Nigerian dictionary.

It would take years to rebuild public trust. President Olusegun Obasanjo’s reforms of the Central Bank and a major banking recapitalisation helped steady the system. The sector began to regain credibility.

It was against this background that the first wave of fintech startups emerged. They weren’t pitching a way to improve trust.

They did something far more subversive: they had ideas of connecting banks in ways the banks themselves had resisted for years. Since the early 1990s, a culture of cutthroat competition had dominated the industry. Banks operated as islands, guarding their systems and customers with a jealous edge. Any change imposed from outside was likely to be met with resistance or ignored altogether.

But that’s exactly what the earliest fintechs pulled off. They challenged the banks' thinking, introduced collaboration in an industry built on rivalry, and expanded the entire market for financial services.

They weren’t missionaries. They did it for the upside. In many cases, they even invited the banks to buy in. Some of the most prominent early fintechs offered equity stakes to the very institutions they were trying to connect.

There are numerous stories to be told about Nigeria’s Fintech Originals, the first wave of fintech startups that helped to show what was possible and went on to build impressive businesses. Some of their stories have become lore, and the tales of the startups that failed early have mostly been forgotten.

This isn’t about nostalgia, but insightful reporting that sheds light on the past and the context around it. Smarter people would also add a line about documentation.

There’ll be eight of these stories in this series (each one will be published biweekly) and you’ll be able to get all of them here. I can’t wait for you to read them. Let me know what you think in the comments!

P.S.

If your company cares about financial infrastructure, inclusion, or the future of digital finance in Africa, this series is open for sponsorship.

It’s a chance to associate your brand with deep reporting, systems thinking, and original insight on the evolution of fintech.

Reply here or reach out: olumuyiwa@notadeepdive.com

See you on Sunday!

Do you commit to finishing this series and not leave the audience hanging?