Dangote Group's disturbing history

Three times is a pattern....

Welcome to the 85 subscribers who joined us last week - we’re almost halfway to our goal of 1,000 subscribers in 6 weeks. If you haven’t already subscribed, fix up!

If I had a dollar for every narrative of fintechs k̶i̶l̶l̶i̶n̶g̶ challenging banks, I probably would not be on Substack, whoring myself and my thoughts in the hopes that someday you guys will fall for it and pay a subscription fee.

“Today, all major Mobile Network Operators have Mobile Money operations, which has become their new cash cow to the detriment of the banks. In some markets such as East Africa, the MNOs, including Safaricom, are operating “banking services” directly competing with traditional banks.” - Africa CAN

Back to the matter at hand: the latest bank challengers are Payment Service Banks (PSBs) and Mobile Money Operators, a.k.a telcos like MTN, 9Mobile and Airtel. It’s easy to understand the argument for banking led by the telcos. Mobile phones are everywhere — estimates say we have anywhere between 99- 170 million mobile phones — so telcos have a real shot at cracking this mobile banking thing.

Plus, banks suck at payments. Banks don’t have many physical branches even in urban areas. Where these branches exist, they’re often crowded while ATMs are frequently out of service. USSD, which can be a lifesaver on some days, is inshallah and vibes on other days.

Why have banks remained so meh? Asides from just handing someone cash, banks were sort of the only way to make payments for years, so they didn’t have incentives to make the experience better for customers. Today, if banks give you any wahala, mobile banking and mobile money agents are ready alternatives, and my word, they have become big businesses. For instance, In this Rest of World article, one agent earns a combined $1,200 (500,000 Naira) in revenue from commissions across his five shops per month.

But there’s one little snag: is it banking if you can’t — drumroll please — give people loans? Because according to Nigeria’s new mobile money regulations, PSBs can’t give loans, advances or any sort of guarantees. The way I see it, this inability of PSBs to give loans will affect CBN’s precious plans to make sure that by 2020, only 20% of Nigerians are financially excluded — the CBN has already failed at this goal, much like it’s failing at managing inflation — but that’s tea for another day.

Not another financial inclusion plan trying to “include” poor people with free debit cards and payments

Hear from the CBN: “Despite several initiatives including the Introduction of Microfinance banking, Agent Banking, Tiered Know-Your-Customer Requirements and Mobile Money Operation (MMO) in pursuit of this objective, the inclusion rate remains below expectation.”

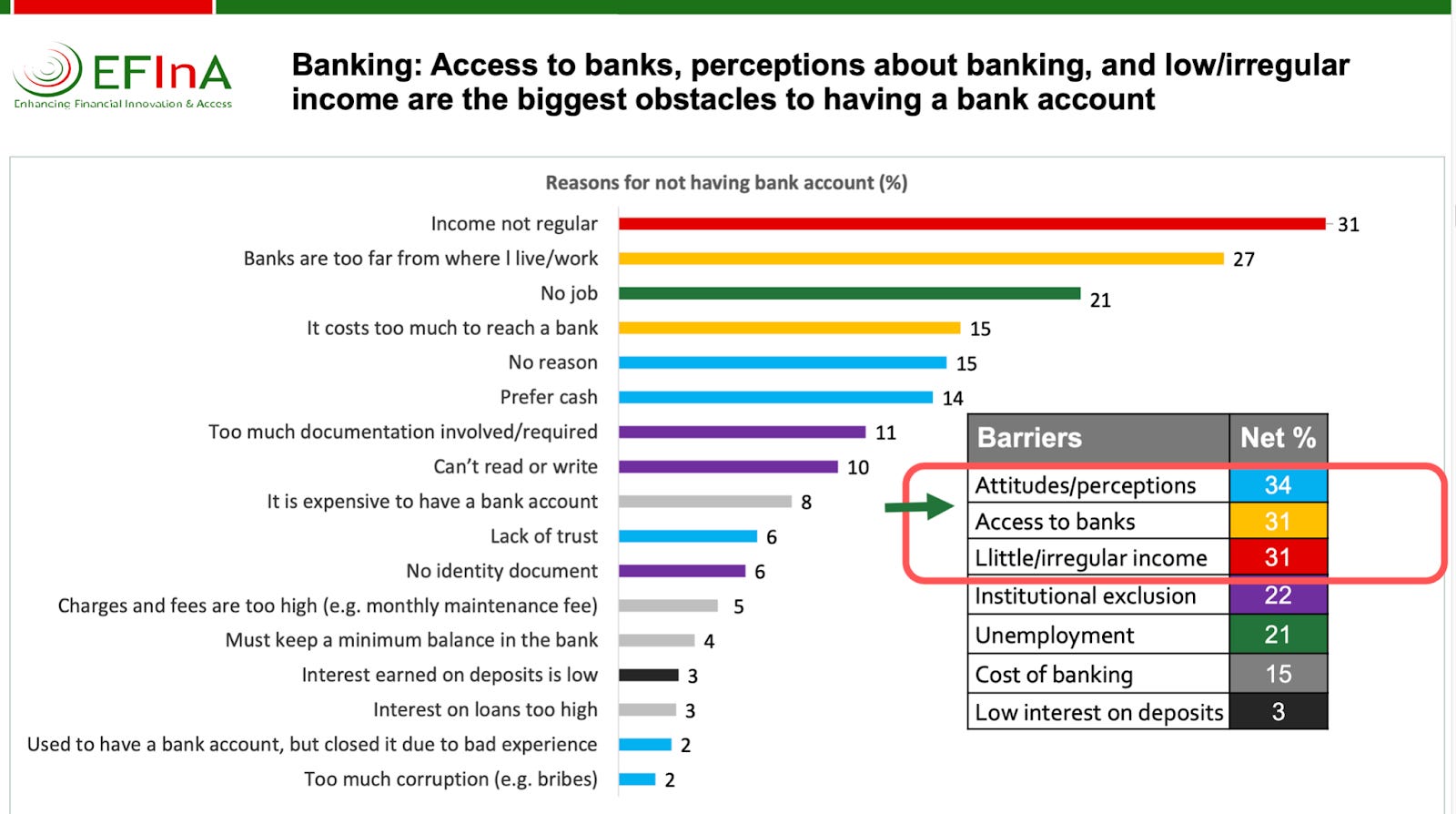

Let’s bring it home: According to EFInA’s 2020 report, some 93% of people in the formal sector have bank accounts so there’s no problem there. The real problem is that Nigeria’s Central Bank wants people who are very poor to care about bank accounts and use financial services. These are mostly people who are dependent on other family members for money. If you think this section of the population is small, think again — there are only 40 million unique Bank Verification Numbers (BVNs) in Nigeria.

As the EFInA report shows, the top reason people don't have bank accounts in Nigeria is that their incomes are not regular. The third reason is that people have no jobs — yes, I’m looking at you President Buhari.

What poor people need to be convinced to use financial services are access to loans that will help set up businesses or expand existing businesses so they can earn regular income. Like I said in my last newsletter, only 2% of people in Nigeria got loans through banks in 2020 and they’re all on my “eat the rich” list.

TL:DR It’s something you already know, poor people need loans and not more debit cards with no money in it and as long as the PSBs and Mobile Money Operators can’t offer loans, it won’t do much to move the needle for financial inclusion.

And since we’re still on the topic of things that won’t move the needle, we’re back to the Nigerian government vs D̶S̶t̶v̶ PayTV.

Nigeria and PayTV prices again…..

In Sunday’s newsletter, I wrote:

Most of that bad blood comes from a long history of Nigerians feeling like they pay too much for DStv subscriptions. There have been attempts to legislate the pricing by the government and you’ll find a lot of Nigerians who swear MultiChoice is a monopoly - it isn’t.

DStv prices across Africa, June 2020 - Credit: The Cable Ng

After MultiChoice - owners of DStv and GOtv - raised prices in response to the Nigerian government increasing Value Added Taxes (VAT), our legislators took one look from their hallowed chambers and said, daz not good. They set up a committee to investigate the price increase and got a report from said committee in February.

Now the House of Representatives has adopted the report which recommends a pay-as-you-go pricing model and price reductions. Adopting the report doesn’t translate to any real changes yet so the House of Reps is kicking the report upstairs to the Federal Government.

Parting shot: “[Pay-as-you-go] is difficult because the content has been created, what you are paying for is access. How you use the access is entirely discretionary and up to you.” - Tunde Irukera, Executive Vice Chairman, FCCPC

We’re ending it on a bit of a heavy note this Friday with something that can only happen in Nigeria.

Dangote Plc’s disturbing history of meeting protesters with armed force

According to People’s Gazette, seven persons are feared dead at Dangote Sugar Company, in Gyawana, Adamawa State owned by Africa's richest man, Aliko Dangote.

Reports indicate that the soldiers opened fire on the protesters around 5pm and so far, it hasn’t caught a lot of attention in the news cycle but it should, because this is something of a pattern for Dangote.

In November 2020, one worker was killed by policemen when some staff of Dangote were protesting unpaid salaries at an Ibeju-Lekki factory. In 2014, seven people were also shot and killed by soldiers at a Dangote Cement factory in Gboko, Benue state — after trying to sweep the matter under the carpet, Dangote eventually paid N5 million each in compensation to the families of the seven deceased persons.

May the souls of the deceased rest in peace, but more importantly, may their families get justice.

That’s enough reporting for one day, here are some of the other interesting things I read this week.

What else I’m reading

A fun drinking game would be taking a shot every time a startup says it wants to bank the unbanked; meanwhile, Stop Saying You Want To Bank The Unbanked

Ways and Means a.k.a “The Central Bank is borrowing the Federal Government wayyy too much money”

Gotta hit this:

We — Yes, we’re in this together now — are trying to hit 1,000 subscribers in the next four weeks and a lot of that will come down to division of labor. That means, I’ll write the awesome content you know and love and then you’ll share aggressively — as those pesky kids say on Twitter.

Here’s how you can help:

Share this post across Social media - Twitter, LinkedIn, Facebook

Drop a link in those annoying WhatsApp groups you’ve muted for a year

Share the link on your office Slack so they can remember you as the person who shares dope stuff — we all love people like this

Leave me a comment and share your thoughts

I’m leaving this for last because if you’ve not already subscribed, wyd??? Come on now, smash that subscribe button and let’s get this show on the road.

What I’m drinking:

Just like Sunday, all I’m drinking this Friday is room temperature water because I’ve got exams on Saturday — damn you, adult education. Drink a beer or two for me this weekend, see you on Sunday!

Sometimes I wonder if anyone in the CBN really gives a hoot about the unbanked. Their actions say they don’t.