For 2021, Emefiele gets a C

The volatility of the Naira is synonymous with Emefiele's tenure

Today’s newsletter is brought to you by GetEquity. GetEquity allows you to invest in some of Africa’s most promising startups so that you can own the next startup unicorn. Learn more about GetEquity here or download the GetEquity app on ioS store and Google Playstore.

We’re on the march to 5k subscribers! Tell your friends and your network about the newsletter and win custom Notadeepdive t-shirts, coffee mugs and hoodies.

If you missed last week’s newsletters, catch up here and here. And if you’re not already a subscriber, let’s fix that right away — you’ll be joining a community of some of the coolest people who know the inside gist of what’s in the news.

Let’s get into it.

Nigeria ends its pointless standoff with Twitter

We spent a lot of time last year criticizing Godwin Emefiele. We dissed Emefiele’s disastrous FX policies, excessive borrowing to the FG and his constant kowtowing to Buhari. Our criticism of Emefiele was so constant, one company abandoned a planned partnership with Notadeepdive as a result — thank you, GetEquity, for stepping in with muscle. The big picture is that Emefiele’s actions are driven by Buharinomics.

Seven months ago, President Muhammadu Buhari banned Twitter after his tweet, which referenced Nigeria’s civil war as a thinly veiled threat to ‘trouble makers,’ violated the platform’s community guidelines. At the time, Buhari claimed that the purpose of the ban was to get some concessions from Twitter. And at the height of the dramatic dance, the country’s Attorney General threatened to prosecute people who kept using Twitter.

So what did Nigeria’s Twitter ban achieve? Late on Wednesday, the Federal Government (FG) reversed the ban on Twitter after months of rhetoric. As part of the reversal, Twitter has agreed to establish a legal entity in the country this year and to comply with tax obligations, according to the government. But this isn’t as important as it sounds. Even without this agreement or an office in Nigeria, Twitter would have tax obligations as the government steps up enforcement of the Finance Act of 2022, which compels companies with a significant economic presence in Nigeria to pay taxes — like we said in Friday’s newsletter. Nigeria will begin collecting these digital taxes in 2022.

Twitter has also agreed to enrol Nigeria in its Partner Support and Law Enforcement Portals, something that could have happened without a seven-month ban. The FG also pointed out that the social media platform has agreed to be respectful to local laws and matters of national security concern.

Taken together, it doesn’t feel like the government gained much from the ban — not surprising seeing as we don’t have a lot of leverage. If we had India’s user numbers (24 million) or strategic importance, it may have been easier to strongarm Twitter, but with our 4 million Twitter users (rough estimate from 2018), it’s an uphill climb.

Instead, Nigeria’s Twitter ban has been a net negative. It shrunk the civic space and wiped away revenue for influencers, brands and ordinary people doing business on Twitter. Government agencies like the National Bureau of Statistics, which used Twitter to update us on inflation rates, obeyed the ban, making it difficult to follow food inflation figures. Even health agencies tasked with sharing critical information about the pandemic abandoned Twitter to comply with the government’s order.

Phishing scammers posing as customer support handles of banks have become pervasive. I spoke to 12 victims of such scams; unfortunately, no bank cared enough to take a break during the ban to educate and protect their customers. Wema Bank violated the ban but only to announce that they were signing Davido as a brand ambassador. So we know it was possible for banks to warn customers if they gave saw it as a problem. I guess they didn’t.

Still speaking of lenders, are reckless debt recovery methods here to stay?

Normalizing reckless debt recovery methods

“There have been a lot of more articles about lenders and public shaming since 2019 but none of the regulators did enough to control these companies currently seem to care. While I will concede that a lot of Nigerians have a curious attitude to repaying loans, there have to be better loan recovery practices to enforce repayment.” - Notadeepdive (July 2021)

In the same week that an ethical debt recovery startup raised $1.7m in funding, another Nigerian digital lender seems to have landed itself in hot water over its recovery methods. Not satisfied with shaming loan defaulters by sending embarrassing text messages to their friends and contacts, lenders have upped the ante. It’s now commonplace to receive Whatsapp messages from lenders shaming defaulters — any hope of NITDA taking action to stamp out these methods has since disappeared.

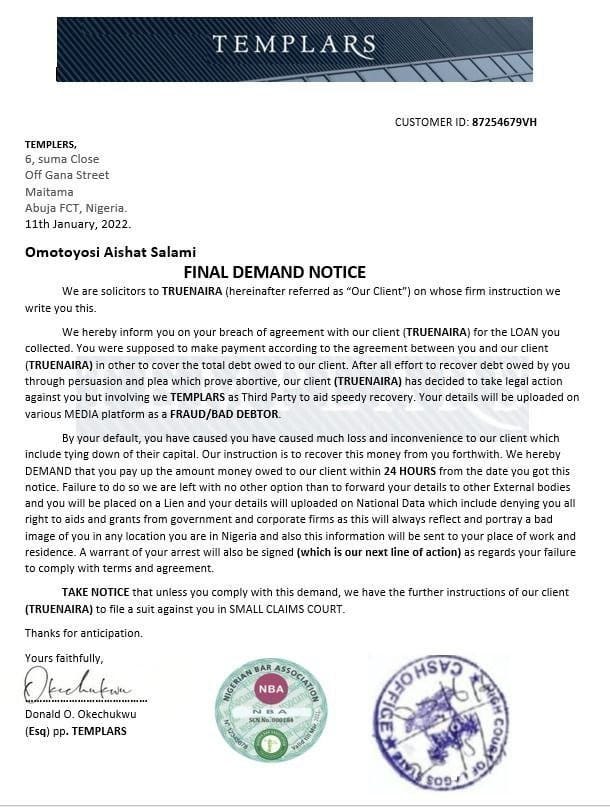

It’s probably why one digital lender, True Naira, reportedly forged a demand letter from the high-profile law firm, Templars. Why would anyone think forging a letter from Templars and opening themselves up to a lawsuit is a good idea?

While Templars have issued a disclaimer distancing itself from the demand letter, the action of the digital lender isn’t surprising. Lenders have been ratcheting up their dubious recovery methods without consequences for years and if NITDA continues to look the other way, things can only get worse from here.

That’s enough talk about digital lenders! We’re introducing a brand new section for the next weeks….

The Signal

This week, one of the world’s most famous accelerator programs, Y Combinator, has decided to increase its cheque size from its standard $125k for 7% equity to $500k. But here’s what caught the attention of investors, founders and other accelerators: $375k of that sum (a follow-on investment) will not be in exchange for any equity immediately. The extra $375k could be critical for startups to get to market and scale their service offering.

The extra $375k funding will be provided under an uncapped Simple Agreement For Future Equity (SAFE) agreement with a Most Favored Nation Clause. Because of these provisions, YC will receive equity at the best valuation and terms when the startup raises additional funding (perhaps in a Series A round).

The most important thing is that startups can now raise capital quickly when they get into YC and this momentum is critical for growth. An extra $375k gives a longer runway to founders, and for YC, these represent better terms, and a stronger pipeline to grow. A few people argue that the new terms only works for YC, but we think it is left to founders to consider the best terms in front of them. For us, we say more funding is often better than none as African startups need more follow-on round investment and scale up capital to grow.

To learn more about investing in Africa’s best startups, download GetEquity now.

Godwin Emefiele’s performance gets global recognition

Nigeria’s Central Bank Governor, Godwin Emefiele, has received a “C” rating from “Central Banker Report Cards 2021: The Art Of Timing”, published by Global Finance. It’s an interesting score, given that the report goes on to highlight the policy failure of the CBN under Emefiele.

“In recent years, Nigeria’s central bank has engaged in deliberate measures to ensure the stability of the Naira. The measures have included a tight grip on the local currency and even halting the sale of forex to bureau de changes…. In many aspects, the volatility of the Naira is synonymous with the reign of Emefiele, which since 2014 has been characterized by rising inflation and tremors in the banking industry.” - Global Finance Report

With inflation at 17.75%, monetary policies that aren’t delivering the expected results and a confusing FX policy, how did Emefiele get away with a grade as generous as a C?

Read more: Central Banker Report Cards 2021

Enough reporting for today, here’s what I’m reading:

What I’m reading

Beyond the happy faces on social media, content creation with families, particularly children, can be complex and fraught with risk

Why Tesla soared as other automakers struggled to make cars

The World’s biggest crypto fortune started with a friendly poker game

Y Combinator’s new deal sparks fear in seed investors (Paywalled)

Edited by: Abubakar Idris

See you on Sunday, and please leave a comment!

On the topic of Digital lenders, in my opinion, just as any new initiative in Nigeria, the microfinance market has gotten saturated quickly, and digital lenders have all thrown caution to the wind (poor credit worthiness profiling) trying to out-disburse one another. Also there is more to Fintech than digital lending, settlements and wallet systems. That is what we at viider consulting (business tech), are looking to achieve (yes I had to throw in my ad) -wide grin-. Also what's a notadeepdive read without some Meffy dragging, lol!

Lovely read as usual!!