Jumia is not a doorstep delivery company

The Jumia story has become smaller and that's the path to profitability

If this newsletter was forwarded to you, subscribe for free:

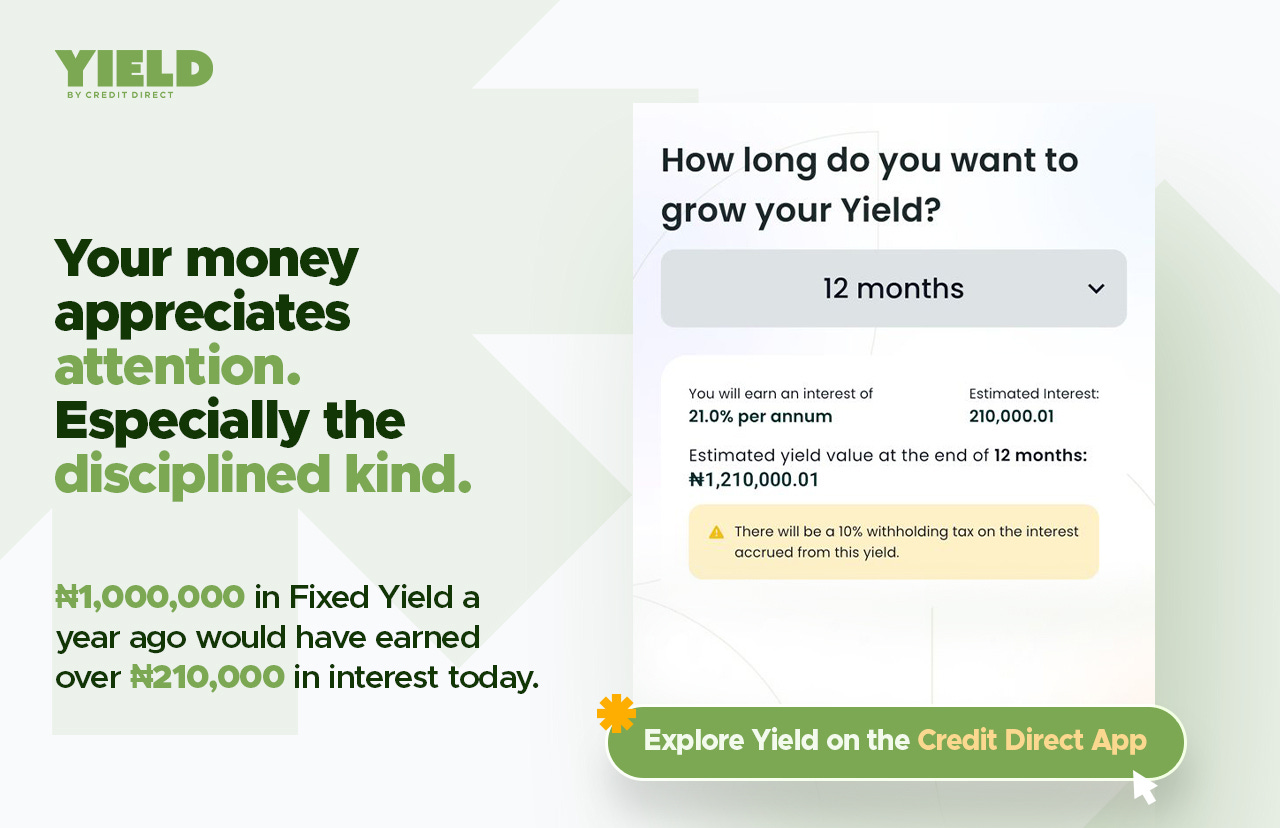

TOGETHER WITH CREDIT DIRECT

You can wait another year, or you can start earning on Yield today.

Jumia is not a doorstep delivery company

The general idea when you think of Jumia is of an e-commerce platform you visit when you want to buy, say, a new phone. You sift through a bunch of really expensive options, pay online, and it gets delivered to your doorstep in a major city like Lagos or Nairobi.

But one part of that picture isn’t completely accurate because Jumia isn’t really a doorstep delivery company. At least not anymore.

In Q1 2026, 74% of Jumia packages were fulfilled through pickup stations rather than door delivery, up from 67% a year ago. So the correct picture is: you go to Jumia, order a phone, and pick it up the same day or a few days later at a pickup station.

Skipping the last mile is a strategic masterstroke for Jumia’s unit economics. They still move products through warehouses and logistics partners, but they no longer have to send a rider to a customer’s address, call three times, and return with the package when the person isn’t home.

It’s a key reason Jumia’s fulfilment cost per physical goods order stayed flat at $2.06 even as volumes grew sharply and fuel prices increased in Nigeria and other African countries.

The mental picture of ordering from Jumia is wrong on geography, too. This is not an e-commerce company selling phones to people in Lekki, Kilimani and Zamalek. In Q1 2026, 62% of Jumia’s orders came from upcountry regions. (By “upcountry,” Jumia means regions outside its densest e-commerce markets. Places like Gaya, Okene, Yenagoa, Owerri, Wurukum, Ekpoma-Eguare and Ogijo.)

In Lagos, walking to a pickup station may be stressful because you have a ton of options. In a secondary city like Okene, where the item you want may be unavailable, overpriced or dependent on a trader who is also waiting for someone else to bring it from Lagos, walking to a pickup station is part of the bargain.

In Nigeria, Jumia added more than 80 pickup stations in Q1 2026, and its distribution network still covers only about one-third of the Nigerian population. Côte d’Ivoire, one of Jumia’s more mature markets, is closer to 60%.

Jumia is narrower, more physical, and more local.

Since taking over in November 2022, Francis Dufay has methodically killed the distractions. Jumia Food and Jumia Prime are gone. JumiaPay is no longer the center of the story; the company will stop reporting Total Payment Volume as a primary metric by Q2..

Physical goods are the business and the path to the promised land of adjusted EBIDATA breakeven by Q4 2026 and profitability by 2027.

The path to breakeven is to make the platform bigger, take more from each transaction, and stop the cost base from growing wildly.

Asked about the path to cash-flow positivity, Dufay said there are no mysterious blockers; “It’s mostly an execution game.” The company has to keep scaling the top line, improve unit economics, and reduce fixed costs in absolute terms.

As part of increasing its top line, Jumia increased commissions and take rates across most of its countries in January 2026.

This is an important shift because, less than two years ago, Jumia was still talking about keeping commissions stable so merchants would keep supplying the platform. Now, Jumia believes it has earned the right to take more because the platform is delivering more volume, better service and better access to customers.

Yet, even commissions and take rates have a ceiling, so it’s good to see that the company is increasing revenue from other business lines.

Marketing and advertising revenue grew 44% to $2.2 million, and value-added services revenue grew to $1.7 million, helped by warehousing fees from higher volumes, especially from Chinese sellers. Advertising revenue is still only about 1% of Gross Merchandise Value (GMV), and management believes there is room for improvement.

The second thing Jumia has to execute on is supply.

A pickup station does not mean much if the things people want are unavailable, expensive or slow to arrive. It’s challenging to have a catalogue that’s good enough with compelling prices.

This is why the international sellers from China and Turkey using Jumia are crucial; gross items sold from international sellers grew 87% in Q1 2026. According to Dufay, the current growth from international sellers is the result of three to four years of work. A new Chinese vendor can take more than a year or two before making a meaningful GMV and margin contribution.

So Jumia has had to convince merchants who don’t know Lagos, Nairobi, Abidjan or Accra to send inventory here. It is slow, operational work but the payoff is that these international sellers help Jumia widen its assortment. They often operate in categories like fashion, accessories and home and living, where gross profit ratios are higher. They also use more advertising and storage services, which means Jumia can monetise them beyond the basic commission.

This version of Jumia, a marketplace where merchants pay for access, storage, visibility and distribution, is one shareholders should care about.

Jumia also has to execute on cost, and because this is 2026, that involves saying AI a lot. On the Q1 earnings call, AI is mentioned 14 times.

Management says AI is being used in cybersecurity, code quality, accounting, HR reporting, logistics, customer service and seller management. Some of this is the usual public-company AI signalling, and shareholders will probably enjoy it for that reason alone.

There’s also more talk of layoffs, with a plan to let 200 people go this year. When Dufay took over at the end of 2022, Jumia had 4,318 employees. By March 2026, it had just over 1,980 employees. Nothing like talking about AI while cutting headcount to excite shareholders.

Costs rose sharply in sales and advertising to $5.1 million in Q1, and management says it views that positively because the spend is going to customer acquisition and engagement on the back of stronger product fundamentals.

There is a delicate balance in play. If you spend too little, GMV growth will slow, but spend too much, and the road to breakeven will continue to stretch ceaselessly into the horizon. Spend badly, and Jumia returns to the old problem of acquiring customers who never come back.

Dufay told analysts that Jumia’s marketing spend ratio is still lower than that of much larger emerging-market e-commerce players, and that most of the budget goes into online channels where spend can be moved daily or weekly if a market is not responding.

So the model is not simply “cut your way to profitability.” That would be easier to understand and less interesting. Jumia is trying to spend more on the parts of the business that drive GMV while cutting the parts that do not need to grow with GMV.

The business that now makes the most sense is not the one with the grandest internet story. It is the one that gets a phone case from a seller in China to a pickup station in Gaya, charges the merchant for visibility, charges for storage, takes a commission, and keeps the fulfillment cost flat.

After years of big promises, the Jumia story has become smaller and therein lies the path to profitability.

How exactly are they going to beat Temu?