Lending Is Easy. Treasury Bills Are Easier.

What happens when the government offers better returns than lending?

If this newsletter was forwarded to you, subscribe here for free:

TOGETHER WITH CREDIT DIRECT

Nobody accidentally builds a great business. The best financial decisions are the ones that keep working long after you stop thinking about them. Credit Direct Business grows your funds at 15% p.a. consistently, without asking for your attention.

You built the business. It should return the favour.

Lending Is Easy. Treasury Bills Are Easier.

One of the recurring ideas I share in Notadeepdive is that lending is easy. You get some funding. Customer deposits, VC money, a DFI facility, whatever is available. You build a credit model, talk about AI in your TechCabal interview, and aim at the gap in your pitch deck: the millions of retail borrowers big banks ignore.

Getting people to repay is where things get complicated. There is no shortage of Nigerian lending startups that raised money, built products, and genuinely believed in their higher calling of serving borrowers the banks wouldn’t touch with a ten-foot pole.

When things go sideways, the founders will tell you the credit models didn’t work, or the macros turned, or collections were harder than expected. All true.

And it’ll lead us right back to why big banks, with their huge balance sheets and cheap deposits, aren’t more interested in lending in the first place. Every year, we have different answers.

GTCO’s FY2025 financial statements show a loan book of ₦3.13 trillion. 85% of those loans went to corporates. Borrowing to starving writers and overworked accountants, a.k.a retail banking, was ₦249 billion. There are fintechs with bigger retail loan books.

Lending to Nigeria’s army of Small and Medium Enterprises was ₦31 billion.

If GTCO isn’t deploying its ₦12.55 trillion in customer deposits into lending, what is it doing with them?

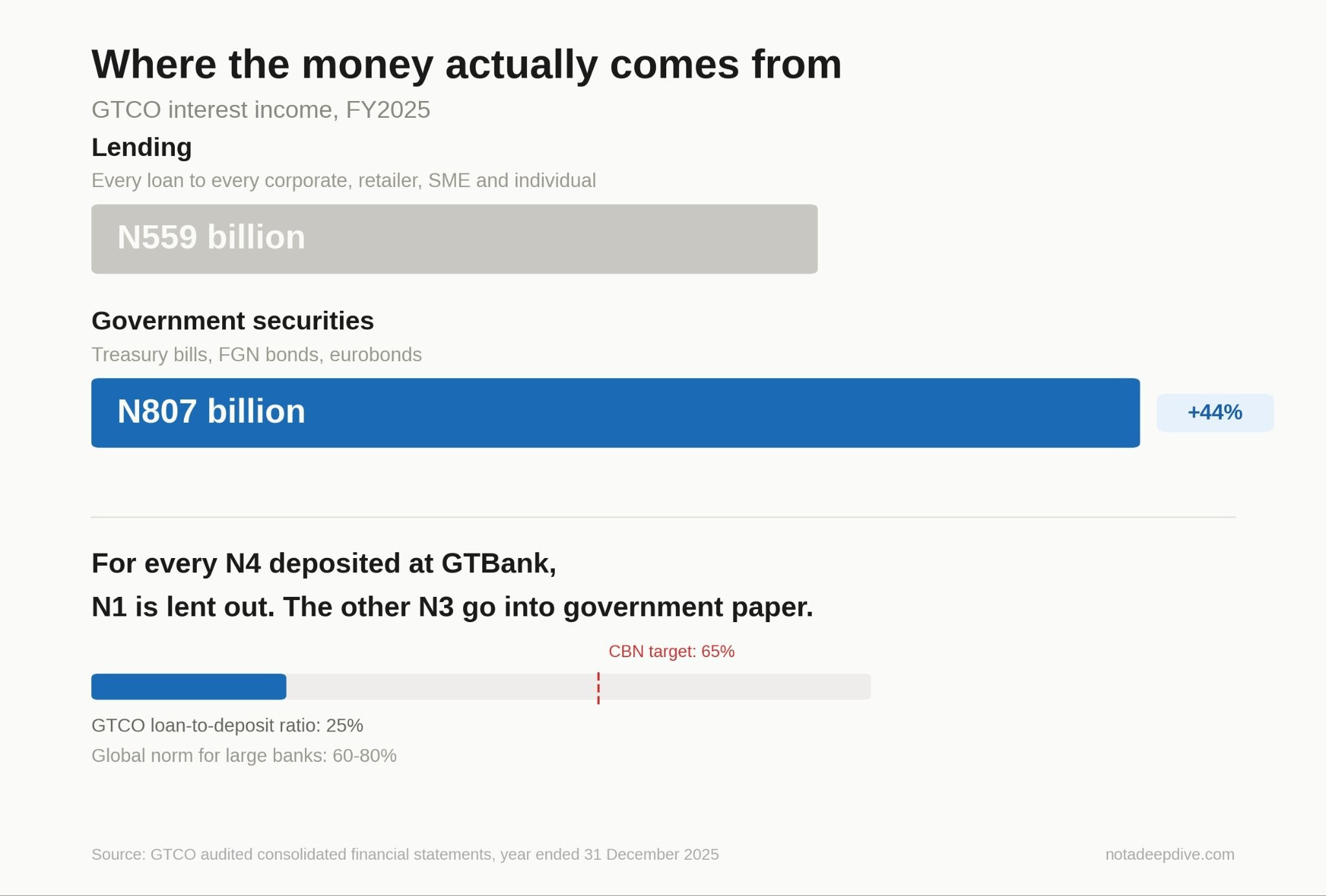

Buying government securities. Treasury bills, FGN bonds, eurobonds, commercial paper — ₦5.54 trillion worth, a portfolio 77% larger than its entire loan book.

For every four naira a customer deposits at GTBank, the bank lends roughly one naira to another customer. The other three naira go into government securities.

GTCO is the most extreme version of this in the Nigerian banking sector. The bank’s loan-to-deposit ratio is 25% despite the CBN’s directive of 65%. Other tier-one banks run higher, though most are still well below the target. In other emerging markets like Brazil, India, and Egypt, a 25% LDR at a top-tier institution would raise eyebrows.

The incentives and market structure show how commonsensical GTCO’s moves are.

A Nigerian Treasury bill maturing in six months yields 20-22% with no credit risk. You buy the T-bill, it pays you on schedule, and you go home.

A corporate loan yields maybe 25-28%. For that extra 3-6%, you take on credit risk. GTCO’s loan impairment charges in 2025 were ₦66 billion. The securities book had impairment charges of ₦114 million. Not billion. Million.

GTCO’s loan book earned ₦559 billion gross, roughly ₦493 billion net of impairments. The securities book earned ₦807 billion gross, roughly ₦807 billion net.

To match what the treasury desk produces from government paper, GTCO would need to add another ₦3 trillion in credit, hire the people to underwrite it, set aside the capital, absorb the defaults. Or it could just buy more treasury bills.

GTCO’s deposit base costs almost nothing to maintain. Retail savings accounts (₦2.99 trillion in deposits) pay low single-digit interest. Corporate current accounts (₦5.57 trillion in deposits) often pay nothing at all. A bank getting deposits at 2-4% and buying T-bills at 22% does not need clever financial engineering.

Banks are not failing to lend because they are timid or incompetent. They are making rational capital allocation decisions and the highest risk-adjusted return available to a Nigerian bank with a large deposit franchise is not consumer credit or SME lending. It is government securities.

There is a version of this argument that is a moral case against GTCO and banks like it. Nigeria needs credit, and banks are hoarding deposits in government paper, starving the private sector of capital.

The banks will respond by asking, “ Who should we lend to?

With 85% of the loan book in corporates, the bank is already lending to the creditworthy part of the economy. When it lends to retail customers and SMEs, the impairment experience is materially worse; retail loan impairments relative to the retail book are significantly higher than corporate impairments relative to the corporate book.

There may not be enough creditworthy private-sector demand to absorb what banks are putting into securities. A T-bill yield of 22% is the government competing for the same pool of capital. At those rates, any private borrower needs to generate returns well above 22% after accounting for risk, and the number of Nigerian businesses that can credibly do that is smaller than anyone would like to admit.

GTCO’s E-business income — revenue from digital transactions, electronic payments, and internet banking — grew 14% to ₦64.7 billion. The bank earned more from digital channels than from lending to retail and SME customers combined.

A final thought.

The 2025 Tax Act introduced withholding tax on short-term investment securities aimed squarely at the income source banks like GTCO rely on most. GTCO’s effective tax rate went from 19.6% to 29.7%.

The bank’s tax bill jumped from ₦248 billion to ₦365 billion and while Profit Before Tax barely moved (₦1.23 trillion), Profit After Tax fell from ₦1.02 trillion to ₦866 billion. The entire decline in profit is tax.

If banks are going to use customer deposits to earn 22% on government paper instead of lending, the government will tax the spread. Whether it actually shifts behaviour is unclear because the pre-tax return on securities still beats the risk-adjusted return on lending.

GTCO declared a final dividend of ₦11.76 per share, bringing the full year to ₦12.76, a 59% increase from 2024 and a four-fold increase in shareholder payouts in three years.

Say what you will, but GTCO’s shareholders will have no complaints.

See you tomorrow!

My major takeaway is underwriting for retail customers needs to be a lot better than it is now!

There are clear infrastructural reasons why this is hard (near impossible)but out of curiosity I’d like to explore innovative solutions that have been deployed elsewhere to tackle this problem.

I’m sure all roads will lead back to the government somehow. Why even bother

Need the dividends to drop ASAP pls. They should help a starving writer over here.