Our offence is that we invested

How Nigeria’s 2008 stock market crash scarred a generation

If this email was forwarded to you, subscribe here for free:

TOGETHER WITH ZEDCREST WEALTH

The Nigerian equities market has evolved significantly over the past two decades. Today, the market is more transparent, better regulated, and increasingly supported by technology that makes investing more accessible than ever before. The next phase of market growth will be driven by greater retail participation, particularly from a new generation of investors seeking long-term wealth creation. The goal, however, isn’t participation at any cost. It’s informed participation.

A money-making opportunity for a generation

In 2007, *Adewole was bent over the day’s newspaper, tracking the closing prices of several publicly listed companies and doing some maths that made him smile. According to the day’s prices, his portfolio was now worth ₦8 million. Two years earlier, he had taken a cautious slice of his pension, the reward for four decades at a public corporation, and put ₦2 million into the market.

He started investing in the stock market almost by accident. His bank, one of the most prominent in the country, was selling shares, and the bank branch had become part of the sales machine. Customers who came in to deposit or withdraw money would be nudged by tellers, account officers, or whoever else was on the banking floor that day to buy shares.

Adewole did not know what a price-to-earnings ratio was or how to assess the strength of a balance sheet. But he trusted his bank, and everyone agreed that stocks were the next big thing.

That Adewole and millions of other Nigerians trusted their banks was quite an achievement.

In the early 90s, “wonder banks” collapsed, taking depositors’ savings with them, and licensed banks had not behaved much better. In January 1998, the Central Bank revoked the licences of 26 banks, including 12 commercial banks because of their “grave financial conditions.”

In January 2006, eighteen months before Adewole sat smiling over his newspaper, the CBN closed 14 more banks that had failed to raise a ₦25 billion capital requirement. The banks that met the new capital requirements emerged with glass towers, new logos, and full-page newspaper ads inviting Nigerians to own a piece of the financial future. For a retiree like Adewole, the pitch was hard to resist, especially once bank stocks began their bull run.

Seasoned investors were more reluctant. They knew a different market where you bought stocks you recognised, kept the certificates somewhere safe, and waited for dividends. This new market would take some getting used to.

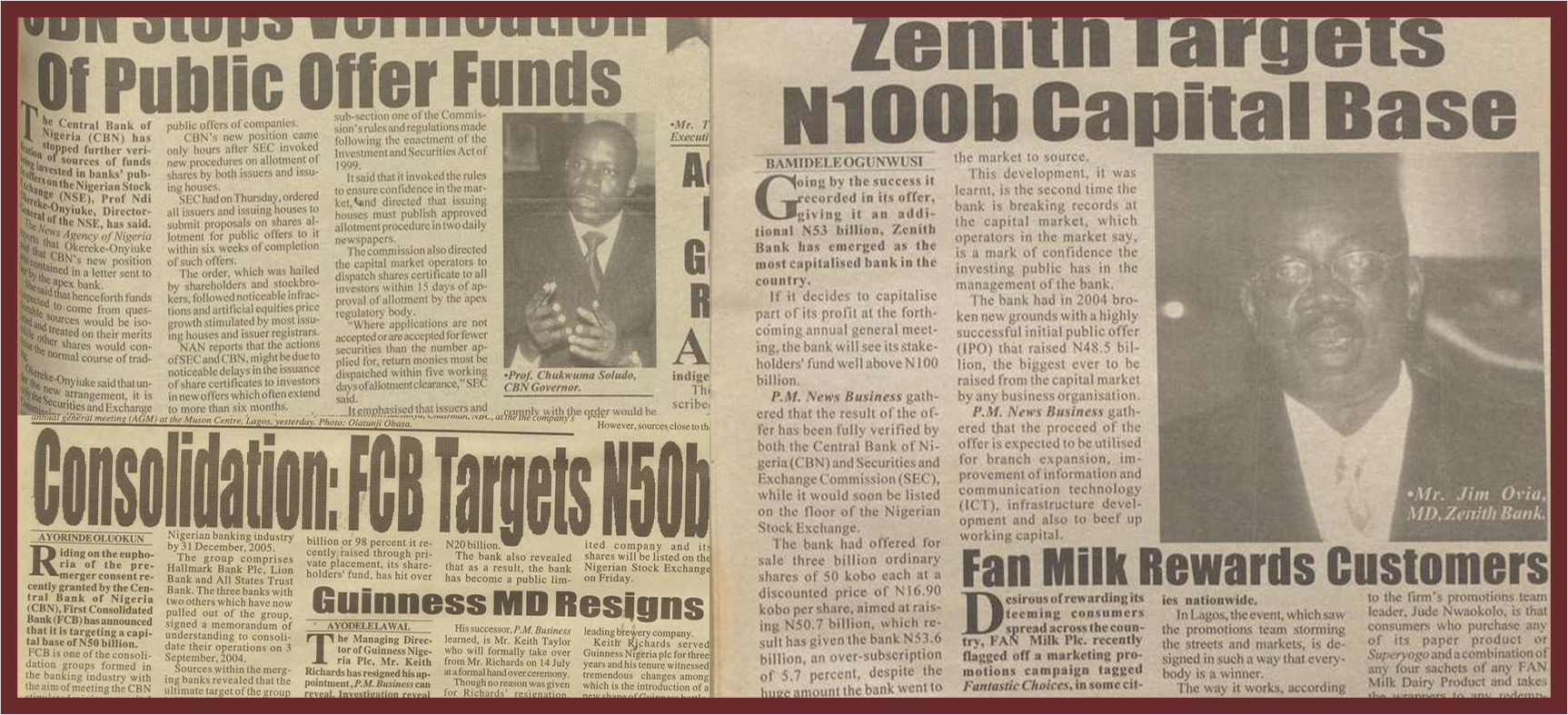

First, the banks needed money

On July 6, 2004, Charles Soludo, one month into his term as Central Bank Governor, told the Bankers’ Committee in Abuja that Nigeria’s 89 banks had 18 months to have at least ₦25 billion of their own money as shareholders’ funds (the cushion that protects depositors’ savings from bad loans). The old requirement was ₦2 billion, and most banks did not even have that.

To survive, 89 banks would need to raise ₦2.2 trillion. The only way out for the laggards who couldn’t dream of raising such sums was a merger.

Soludo believed that Nigeria didn’t have banks big enough for its economy.

The oil boom of the 2000s created billion-dollar energy projects, and Nigerian banks were too small to lead the financing, leaving foreign lenders like BNP Paribas, Citibank, and WestLB to profit from the economic expansion.

Yet, Soludo also understood what happens when you order 89 banks to find ₦25 billion each in 18 months. Some would raise real money, but others would try to cut corners. So he promised a “risk-focused, rule-based regulatory framework” in which arbitrariness would be “reduced to the barest minimum.” The Central Bank would publish the names of qualifying banks on December 31, 2005, verify every naira raised, and punish operators who broke the rules.

The recapitalisation had a second goal of burying the memory of the 90s bank failures. Big banks, the thinking went, were safe banks.

By the December 2005 deadline, only 25 banks were left standing. Getting there required the biggest fundraising Nigeria’s capital market had ever seen.

Euromoney reported ₦406 billion raised domestically in 2005, with more than $650 million from international investors. The Nigerian Stock Exchange was busy with new listings, rights issues, and follow-on offerings through 2005 and 2006, and the brokers underwriting it all got rich.

Many of these capital raises were exactly what they said they were, with real money from institutional and retail investors who wanted to own a piece of bigger, safer banks. Others were something stranger.

Afribank had used depositors’ money to buy 80% of its own public offer, paying ₦25 per share for stock that was trading at ₦11 on the Exchange. The shares later fell below ₦3.

Intercontinental Bank had raised 30% of its share capital with depositor funds. Oceanic Bank’s CEO ended up controlling more than 35% of the bank through Special Purpose Vehicles financed the same way. A significant part of the consolidation had been a sham.

Sanusi Lamido Sanusi, who became Central Bank Governor in 2009, shared the findings in a 2010 convocation lecture at Bayero University in Kano after CBN auditors examined the wreckage.

The verification process Soludo publicly committed to in 2004 had, in Sanusi’s words, been stopped “for some unexplained reason.” Central Bank officials had raised concerns with their own senior management at the time, and the Nigeria Deposit Insurance Corporation (NDIC) had documented its worries and pressed for action. Both were ignored.

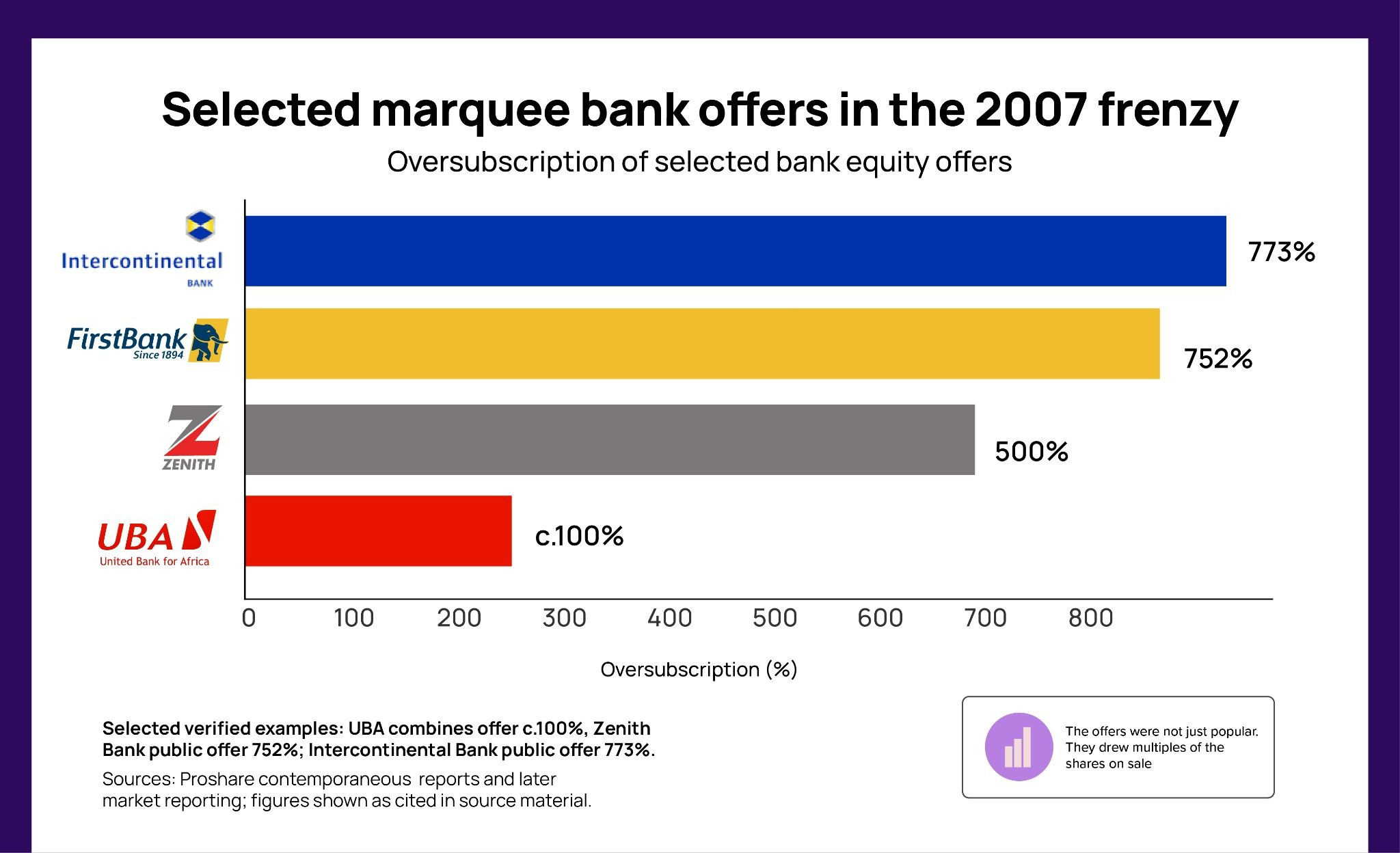

By the end of 2007, the market capitalisation of the 25 surviving banks had grown ninefold, and they accounted for 60% of the entire Nigerian Stock Exchange. Banks took almost all the money raised from the market that year, as new issues soared from ₦552.78 billion in 2005 to ₦2.4 trillion in 2007.

It was a rising tide that lifted all boats. Banks and brokers booked interest income, the issuing houses collected their fees, and Soludo could point to all the activity as proof the reforms had worked. By April 2007, Nigeria had 246 registered brokerage firms, up from the small club that existed before consolidation.

The success then traveled overseas when Soludo was named African central banker of the year and the Nigerian Stock Exchange was called the world’s best-performing bourse.

Every time he opened a newspaper, Adewole saw good news. At that point, there was nothing else to see.

Then came the loans

By 2007, people like Adewole who had bought bank shares could take loans to buy even more shares. So you would put up your ₦2 million in shares as collateral, and the bank would lend you another ₦2 million to buy more. When share prices rose, you could sell some of the shares, repay the loan, and keep the difference.

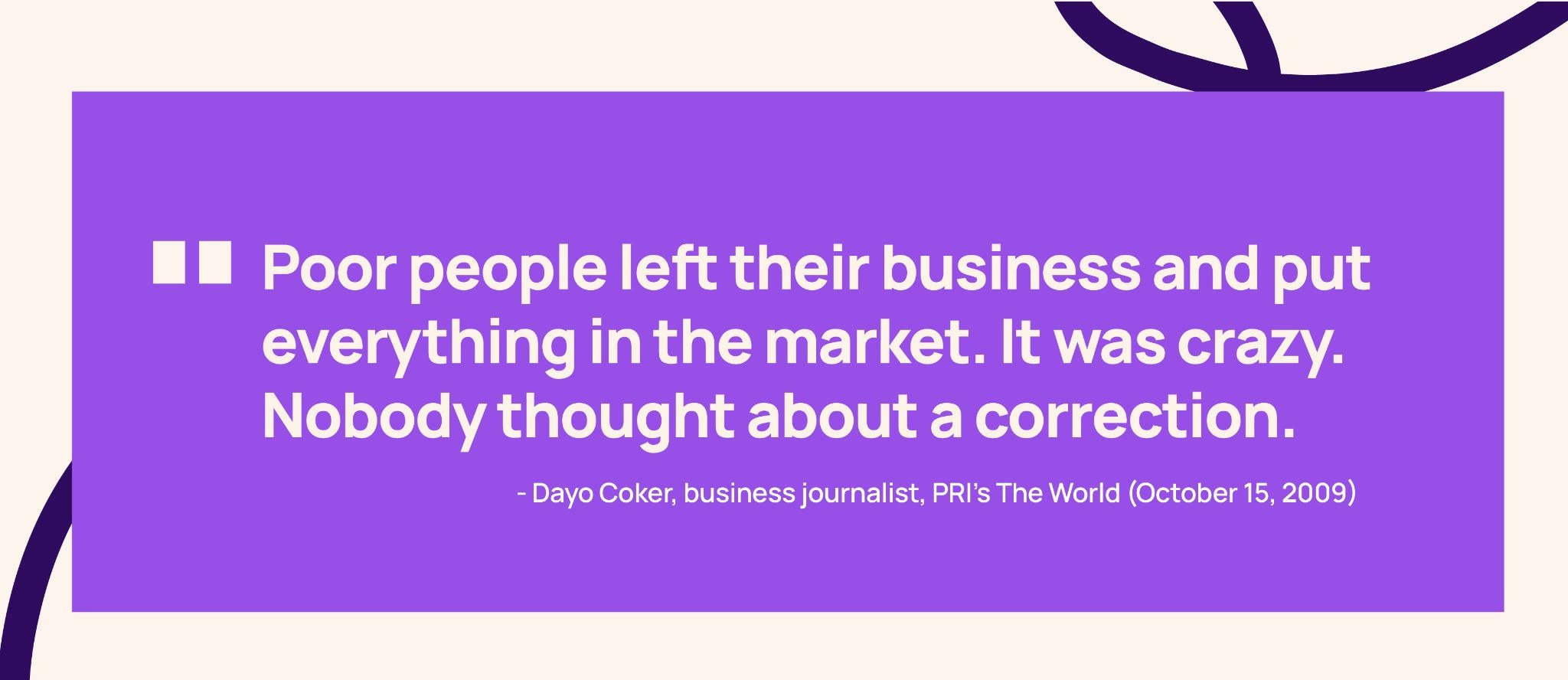

It was hinged on the presumption that prices would keep rising, and for a while they did. Every price increase made the collateral worth more, which justified more lending, which put more money into the same shares, which pushed the price up again. It was roundtripping of epic proportions.

By the end of 2008, the banks were carrying ₦1.2 trillion in share-backed loans, of which roughly ₦400 billion were direct margin loans to individuals and stockbrokers.

The exposures ran through the biggest names in the industry: Intercontinental, GTBank, Ecobank, First Bank, UBA, Diamond, Union, Stanbic IBTC. Some of it was margin lending to retail customers, while the rest was to corporate clients. The banks and their customers would be fine as long as the share prices stayed up.

Olutola Mobolurin of Capital Bancorp described the mechanism perfectly. Stocks were sold to people who were made to believe that prices would never come down. Margin loans were given to buyers who did not know that a falling price would wipe them out.

Adewole was one of them. He held shares he had bought from a bank alongside a margin loan the bank had given him to buy more of those shares. Because the shares themselves were the collateral for the loan, when the price fell, the value of the collateral fell with it, and the bank could call the loan, which would force him to sell the shares to repay it, pushing the price further, and causing the bank to call in even more of the loan.

He could never have seen this coming from just reading the newspapers.

The people behind the scenes

Peter Ukuoritsemofe Ololo was a chartered accountant and licensed stockbroker who studied accounting at Ahmadu Bello University and spent more than a decade at Union Bank and ICON Limited before starting Falcon Securities in 1993. The Wall Street Journal described him as a once high-flying stockbroker for Nigeria’s biggest banks and wealthy individuals, a man who drove himself in a Peugeot 307 while, on some days, his firm accounted for 40% of trading volume on the Nigerian Stock Exchange.

By the boom years, Falcon was the brokerage, and Ololo was the market maker, and being the biggest buyer and borrower gave him leverage nobody else had.

Companies in which Ololo was a director or major shareholder borrowed more than $700 million from five banks, an incredibly large exposure in a fragile system. Separately, the CBN’s debtor list put the exposure incurred through Falcon Securities at ₦88.3 billion, making Ololo the largest individual debtor to three failed banks.

According to EFCC testimony at a Lagos High Court in 2014, a Falcon Securities account was opened with a zero balance to receive a ₦15 billion credit line; another ₦15 billion went to Falcon for the purchase of blue-chip stocks on the floor of the Exchange. The case was still being tried in 2015, and no final public judgment is available.

In a separate matter, Ololo, Adigwe and six others pleaded not guilty to a 36-count charge of conspiracy, stealing and receiving stolen property; that case, too, had reached no verdict by 2015.

According to the Wall Street Journal, when a bank wanted its share price moved, an executive would call Ololo and tell him to buy or sell, and other traders would follow his lead. The EFCC named Ololo in two cases, alleging he had conspired with Sebastian Adigwe of Afribank and Bartholomew Ebong of Union Bank, “by fraudulent means to manipulate the market price” of both banks’ shares.

If Ololo was the broker the banks used, Erastus Akingbola was the bank. He had founded Intercontinental, built it into one of Nigeria’s five biggest, and given it the face of a modern institution with hundreds of thousands of shareholders.

In one EFCC account, Intercontinental issued three cheques totalling ₦10 billion in May 2009 to Tropics Securities and related entities, for shares said to have been bought on the bank’s behalf. Investigators said Akingbola held substantial interests in those same firms. The EFCC alleged he had used ₦179 billion to buy Intercontinental’s shares and prop up its price.

This was a world of dealings Adewole knew nothing about.

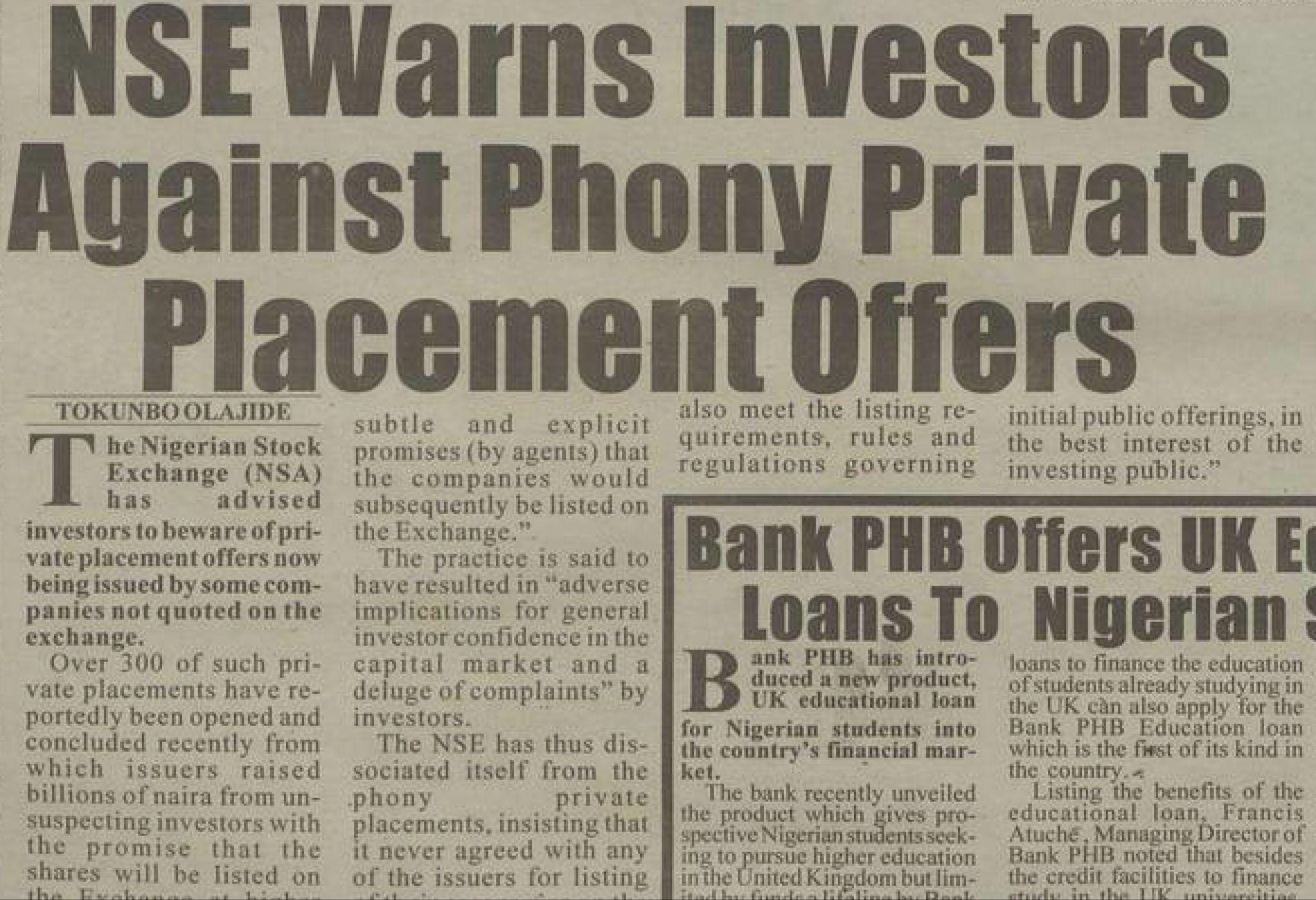

In yet another world, there were private placements that allowed you to buy company shares before they listed on the Exchange. The belief was that once the shares were listed, the public would chase them, the prices would rise, and people who got in early would get rich.

Between 2004 and 2008, roughly ₦650 billion was raised across some 300 private placements, and many of the companies involved never publicly listed.

More than a decade later, Mary Uduk, then the SEC’s acting director-general, told a conference at the University of Lagos that many private companies had exploited gaps in the law during the boom, promising investors public listings they never intended to pursue. She singled out BGL Plc, formerly Banc Garanti, a capital market operator that raised money and never brought its shares to the Exchange.

Other companies gave reasons for not listing.

ARM Properties raised ₦5.675 billion in August 2008, with a listing planned for the fourth quarter. By 2009, its board had postponed the listing, saying the market could not give investors fair value, and the company eventually surfaced on the NASD over-the-counter market as Mixta Real Estate.

Geo-Fluids opened a ₦12 billion placement in May 2008, with shareholders approving a listing the following year, but management found the market too tepid, and the shares did not trade until 2013. Aquitane Oil & Gas sought another ₦15 billion in June 2008, and there’s no account of what became of the offer.

Whether a company never meant to list or didn’t manage to, investors were stuck with shares that could not be sold.

Starcomms’ private placement opened on June 3, 2008, and closed the same day, offering 4.95 billion shares at ₦13 each, with Stanbic IBTC and Chapel Hill Denham as joint issuing houses.

It listed on the stock exchange in July at ₦13.56, fell to ₦7.46 within two months, and ended the year at ₦3.86. Chapel Hill later said that several investors never even read the private placement memorandum. Many bought through brokers and friends who were among the invited investors, without seeing the documents or understanding that Starcomms had been sold as a growth stock expected to lose money in 2008, turn profitable in 2009, and pay dividends in 2010.

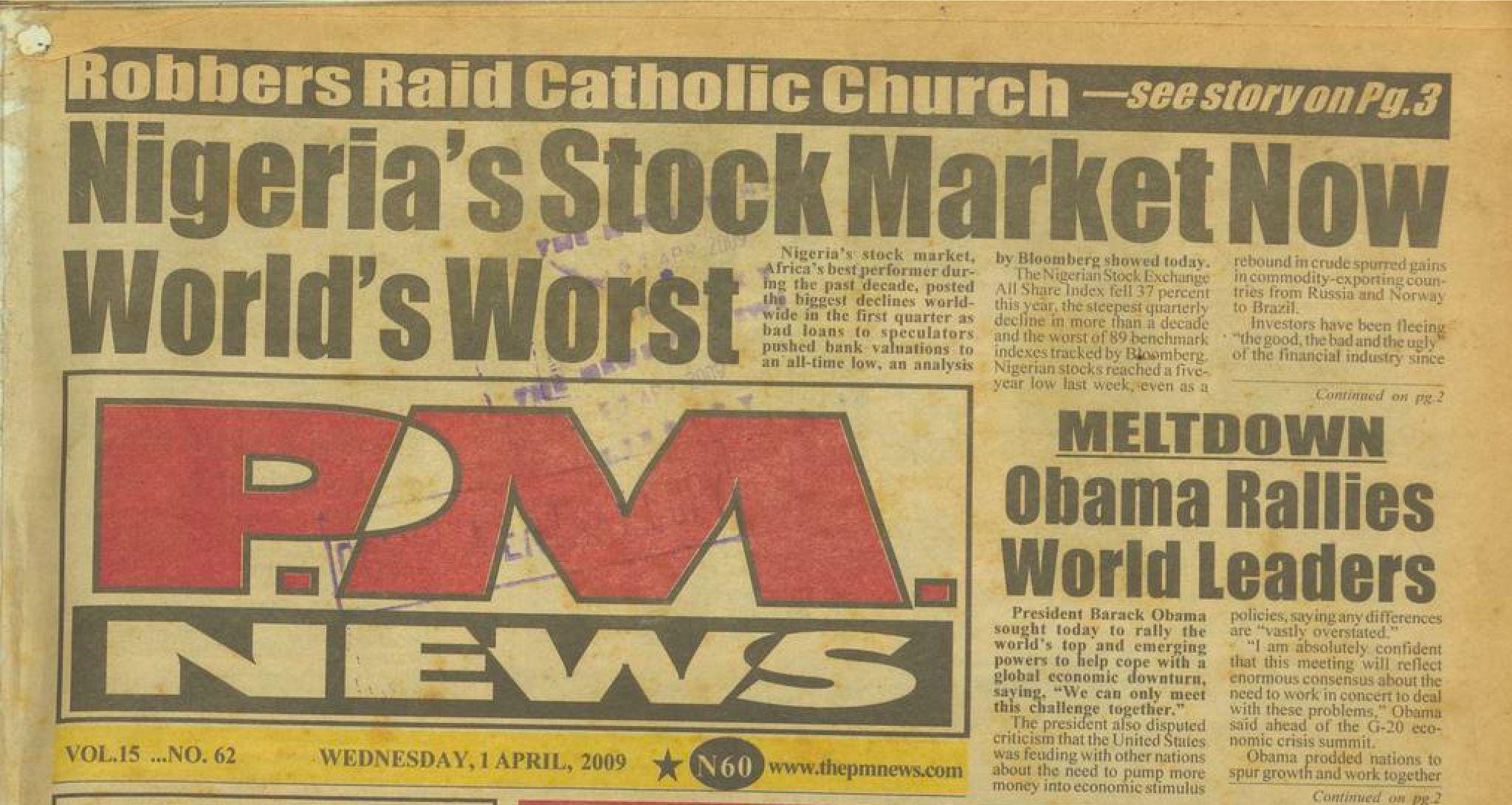

The crash

In April 2008, Meristem Securities published a report in BusinessDay: The Nigerian Stock Market Crash: Coming Soon?

That same month, stockbrokers started calling the clients who had borrowed against their shares to let them know the banks wanted their money back. If share prices were still this high, the customers asked, why couldn’t the banks wait? No one had a clear answer. The brokers’ instruction was to repay or sell, usually within days.

Most people had no cash because everything was in the shares, so they were forced to sell. Those sales caused prices to fall, and by the end of April the All-Share Index had declined from 66,121 to 60,339, nine percent in four weeks. Many interpreted this as a market correction.

So when the index edged back to 60,570 in May, it seemed like the worst had passed, so some clients bought more. The bounce lasted three weeks.

June closed at 54,905, and July slid further to 50,422 even as CBN governor Soludo assured the public that with crude at $147 a barrel and reserves at $64 billion, there was nothing to worry about.

Throughout public addresses in July and early August, Soludo claimed Nigerian banks were insulated from the global financial crisis because their fundamentals were great. The market wasn’t buying it, and prices continued to slide.

On August 28, the Federal Government called a meeting in Abuja and invited the Central Bank, the Securities and Exchange Commission, the Nigerian Stock Exchange, and the major brokerages.

The meeting resolved on a range of measures to arrest the stock market slide. The SEC would halve its fees, and the CBN would lower its monetary policy rate, its cash reserve requirement, and its liquidity ratio. Banks would restructure margin loans through 2009, giving them time before recognising bad loans.

Crucially, the Nigerian Stock Exchange changed how much a stock could move in a day. Up, five percent. Down, one percent.

It would take months for a stock price to halve given the one percent rule, and until it did, buyers weren’t interested in paying these artificial prices.

Through September and October 2008, investors who tried to sell shares could not because there were no bids.

In October, the Exchange bowed to common sense and removed the one percent rule. The official explanation was that it didn’t align with international practice, but the backlog of unfilled sell orders had become unmanageable.

With the rule gone, the air went out of the balloon at once. The All-Share Index opened in October near 46,000 and closed at 36,325, a decline of more than twenty percent. By November 28th, the index was at 33,025. By December 16th, 28,085.

Over sixty per cent of the three hundred-odd securities listed on the Exchange were on constant offer. At every price, sellers outnumbered buyers. No matter the price they were looking to exit at, shareholders could not get out.

Adewole was one of them. By the end of 2008, he had stopped opening the newspaper. His shares were worth a fraction of the loan they secured; the bank wanted its money, and there was no cash and no buyer. So the bank took the shares, millions of them, as unsellable in their hands as they had been in his.

In June 2009, President Yar’Adua replaced Soludo with a new central bank governor, Sanusi Lamido Sanusi, who ordered the Central Bank and the Deposit Insurance Corporation to open the banks’ books together.

On August 14 2009, Sanusi announced that five banks: Afribank, Intercontinental, Oceanic, Union Bank, and Finbank, were insolvent. The five banks had ₦2.8 trillion in loans. Almost half of the loans (₦1.14 trillion) were non-performing, with another ₦456 billion in margin loans.

Sanusi sacked all five chief executives. Erastus Akingbola of Intercontinental, Cecilia Ibru of Oceanic, Bartholomew Ebong of Union, Okey Nwosu of Finbank, and Sebastian Adigwe of Afribank.

In October, three more chief executives at Bank PHB, Spring Bank, and Equatorial Trust Bank were sacked. The CBN then injected ₦620 billion into the rescued banks, some two and a half percent of Nigeria’s 2010 GDP.

Eight days before Akingbola was sacked, Aliko Dangote had been elected the seventeenth president of the Council of the Nigerian Stock Exchange.

At the time of his election, Intercontinental Bank alleged in a petition that Dangote’s companies owed it ₦35.8 billion—Dangote denied owing the bank. Either way, a bank listed on the stock exchange was publicly calling the Exchange’s President a debtor. In August 2010, the SEC removed him, along with the Exchange’s director-general.

Of the eight sacked bank chiefs, only Cecilia Ibru was initially convicted in 2010 after she was charged with twenty-five counts of bank and securities fraud. She entered a plea bargain, and the charges were reduced to three. Francis Atuche of Bank PHB was later convicted in 2021, with the conviction upheld by the Court of Appeal in 2022.

On October 8, 2010, Justice Dan Abutu of the Federal High Court in Lagos sentenced her to six months on each count, running concurrently. She served a prison term of six months and forfeited 199 assets, including properties in Maryland (USA), Lagos, and Dubai, shares, and over ₦190 billion in cash. About $7 million was realised from the sale of sixty-one of those properties, and $3.27 million was transferred to the Asset Management Corporation of Nigeria.

Erastus Akingbola fled to London on the day Sanusi sacked him and stayed there for about a year. In 2010, under threat of extradition, he returned to Nigeria and pleaded not guilty. The case was reassigned to a judge named Charles Archibong, who dismissed the charges and barred prosecutors from trying Akingbola again.

The National Judicial Council later compulsorily retired Archibong, primarily for what they termed his mishandling of the case. The Supreme Court would overturn Archibong’s judgment six years later.

Sixteen years after Akingbola was first charged, his case has yet to produce a verdict. At least fifteen judges have handled it, and one of his lawyers has died of old age.

Peter Ololo, the broker whom other brokers called “Market,” was arrested twice in 2009 and released on bail. His lawyer, Femi Falana, told the Wall Street Journal in December that year: “He was simply managing the stocks. When the shares were going up, everyone was happy. Now that the shares are falling, he can’t be blamed for that.” As of 2014, the trial was still being adjourned, and there’s no public record of the courts reaching a verdict.

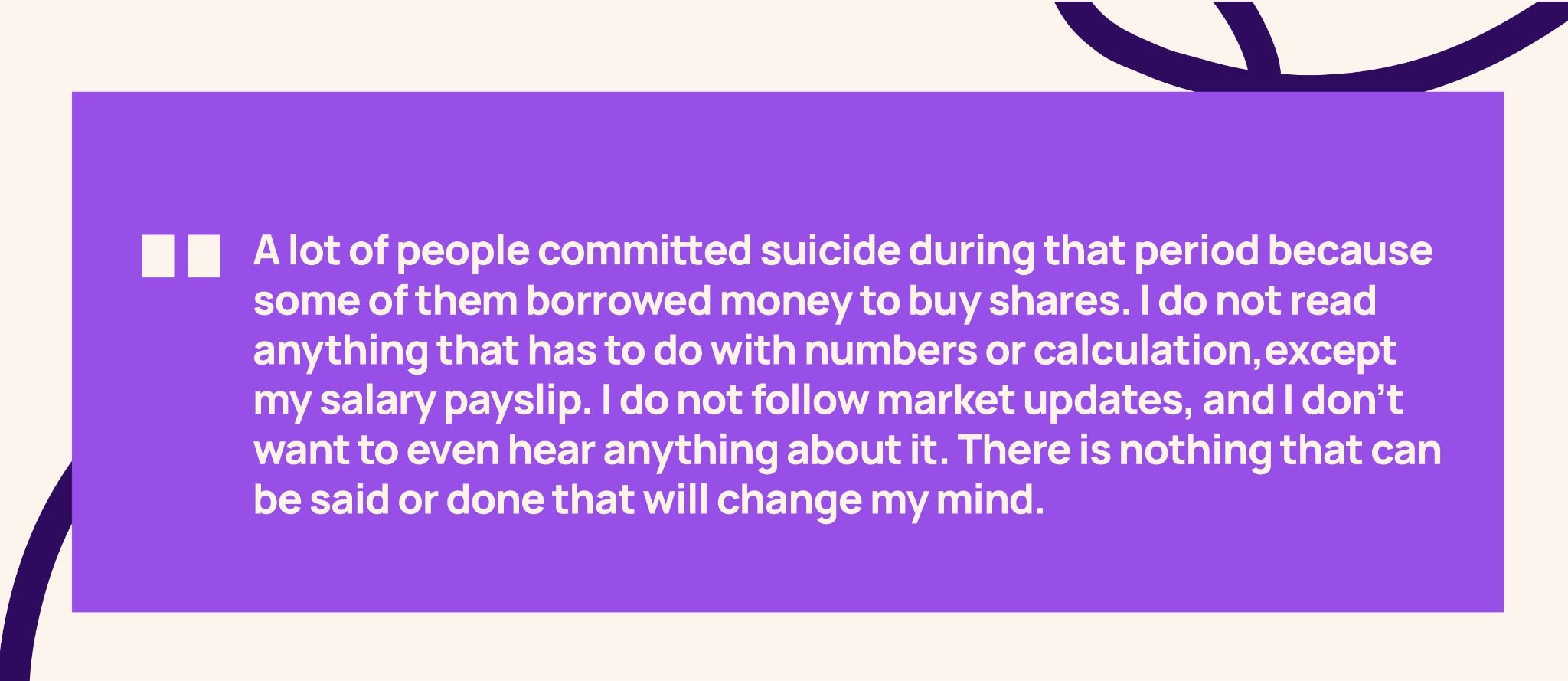

In May 2019, a reporter from the Punch found a 69-year-old man named Abraham Owoeye selling plumbing materials, roofing sheets, and cement out of a small shop in Lagos. In 2004, he had been talked into buying ₦3 million in shares. By 2009, the shares were worth a fraction of that. Eleven years later, his dividends still sat unclaimed at the registrar.

By December 2018, unclaimed dividends in the Nigerian capital market had soared to ₦129.62 billion.

Some shareholders had died, others had bought shares in different names. Some could not be bothered to fight through registrars, indemnities and paperwork for dividends that now felt too small to justify the trouble.

Many, like Owoeye, had simply moved on from the market.

“I just decided not to think about it because at 69, I have realised that there is more to this life,” Owoeye said.

In March 2026, the All-Share Index of the Nigerian Stock Exchange crossed 200,000 points for the first time in its history. For anyone who had stopped checking in 2008, it was just another number.

Adewole Peter wouldn’t have opened the paper for it. Abraham Owoeye, who was selling plumbing materials in Lagos eleven years after the crash and refusing to read anything with numbers in it, wouldn’t have cared. A chart can go back up, but a person may not.

The market has had two strong years, with pension funds looking at equities again and foreign investors buying Nigerian assets. A new generation of retail investors is investing in a market that is no longer as mysterious as it used to be.

It is a better market than the one that found Adewole at his bank branch and sold him shares he didn’t fully understand.

The Central Bank of Nigeria is not where it was in 2008. In the last year, it has pushed banks to recognise the cost of old regulatory forbearance, restricted dividends for affected banks, and asked lenders to stress-test their books.

It’s not that the CBN has become incapable of failure; after all, regulators always look strongest between crises. Rather, it is more that some of the things that were hidden in 2008 are harder to hide now.

The Securities and Exchange Commission is also less sleepy. In 2026, a handful of stockbrokers were penalised for infractions that included false trading and trades capable of creating artificial prices.

When UBA and Access did not pay final dividends for 2025, investors sold. The share prices moved the way share prices should move when shareholders realise that reported profit and cash in their accounts are not the same thing. This is the healthier version of a market that punishes disappointment and reads regulatory circulars. It asks whether profit can survive provisioning, and notices when a bank cannot turn earnings into dividends.

But memory does not move with the index. The people who were burnt in 2008 weren’t sitting at home waiting for better disclosure standards. They still aren’t.

Their market thesis is simply “never again.” They lost the belief that the market was a fair place to take risks as they watched banks sell shares, lend against those shares, use those shares as collateral, then seize the shares when the prices fell. They watched brokers talk confidently until the phones stopped ringing. They watched private placements promise future listings that never came.

And they watched bank chiefs walk in and out of court years later, while ordinary investors adjusted their lives around the hole left in their savings.

So today, the question is not whether the stock market can create wealth or not. It can. The question is whether the next Adewole enters it differently and with more information.

About Sponsored Notadeepdive editions

Sponsored Notadeepdive essays are commissioned by ambitious companies we carefully choose to work with. They support the kind of long-form business stories that are researched, thoughtful and useful to readers.

The essay is held to the same standard as every other Notadeepdive edition.

For questions or feedback about sponsored editions, email me at olumuyiwa@notadeepdive.com.

Today’s Notadeepdive was brought to you by Zedcrest Wealth.

Alongside access to the market, Zedcrest Wealth invests in investor education through the Zedcrest Wealth Academy, expert market insights, and stock recommendations that help people make decisions based on understanding rather than excitement or FOMO.

Take Your Position is our invitation to actively participate in the market with clarity, confidence, and conviction.

Edited by: Yahaya Hassan, Ikenna ‘BFG’ Sam-Ejehu

Graphic design and direction: Adeyemi Bamtefa

Newspaper screenshots: Archivi.ng

more sponsored editions! 👏🏽

This was quite insightful. I bought into the Geo-Fluids private placement then and got my fingers burned. It has made me a much wiser investor now.