What the CBN cannot do does not exist

Does the CBN have the powers to freeze the bank accounts of fintechs?

When I said at the beginning of August that the goal was to hit 2,000 subscribers at the end of the month, it felt a little crazy, but here we are, just shy of 1,400 subscribers. Dare I hope for a miracle that takes us to 2k subscribers in the next couple of days?

If you haven’t already subscribed, c’mon now, do it for world peace.

This is Nigeria. Anything you see, take it like that.

It’s so difficult to defend Nigerian regulators. One minute, you’re telling your timeline how regulation protects consumers from companies that want to take advantage of them — the next minute, the CBN does something so ridiculous, it makes you update your Twitter bio to something like, “tweets are not endorsements”. On Tuesday, a court judge ordered the freezing of accounts belonging to companies that allow Nigerians to buy foreign stock (tech people call them wealth tech companies). RiseVest, Chaka, Bamboo and Trove are some of the companies affected by the judgment.

Here’s what the CBN’s lawyers told the Federal High Court:

These wealth-tech Companies are operating without a license

They are “utilizing FX sourced from the Nigerian FX market for purchasing foreign bonds/shares”

Their activities affect the exchange rate of the Naira to the dollar - I wish I was making this up

CBN’s logic here is a little wonky — some of these companies have operational licences from the Securities and Exchange Commission (SEC). But the bigger issue is that in blocking the accounts of these companies for 180 days, it used an instrument that should be granted only on specific grounds — an ex parte motion. It’s about to get a little complex so stay with me here.

An ex-parte order is typically granted without hearing the other side. Courts should only grant these orders where the party applying for it has shown that irreparable damage will be done to them if the court does not grant the order. Yet, according to the Federal High Court Rules, an order made on a motion ex parte should not last for more than 14 days. This recent ex-parte order to CBN was granted for 180 days.

Where have we seen this before? In November 2020, the CBN secured an ex-parte motion to block the accounts of 20 promoters of EndSARS for 90 days. And in August 2020, the CBN instructed banks to block all transactions on the accounts of betting companies in Nigeria. The betting companies were accused of disrupting the financial system.

How is the CBN getting these orders from the court contrary to the existing rules? Section 97 of the Banking and other Financial Institutions Act (BOFIA) 2020 allows the CBN governor to apply for ex parte motions from the Federal High Court if he believes that transactions undertaken in any bank account with any licensed bank may involve the commission of any criminal offence. There is also no limit to the duration that the order can last.

In fact, the CBN Governor can ask the Federal High Court for an order for continued freezing of the account if the Nigerian Police, Drug Law Enforcement Agency or any other law enforcement agency cannot complete its investigations within the stipulated period of the court order.

TL;DR: What your CBN Governor cannot do, does not exist.

The bottom line: Since our resident travel blogger came into power, executive powers have widened. It has allowed government agencies to make questionable decisions; CBN and the National Communications Commission have been the biggest culprits.

It is worrying that the judiciary is becoming a tool to fight whoever any government agency decides to pick a fight with. Today, it’s these fintech companies, tomorrow, who knows?

And since we're still on the subject of the courts…

This loan company will finally pay for shaming defaulters

My second newsletter was about digital lenders in Nigeria and how they have perfected the art of shaming people who default on loans. Here's what I said at the time:

Digital lenders will tell you that under the current Nigeria Data Protection Regulations (NDPR), they can and will ask you for permission to your data - which I mentioned on Friday - but what they do not mention is that they do not have the right to text your contacts. It’s also super curious that this trend hasn’t gotten the attention of the National Information Technology Agency, given that they investigated Truecaller for a similar privacy issue in 2019.

Thankfully, beyond trying to stifle the technology sector, NITDA has woken up to some of its responsibilities. The agency has fined Soko Lending Agency ₦10m for privacy invasion.

According to NITDA, "This action was taken after receiving a series of complaints against the company for unauthorised disclosures, failure to protect customers’ personal data and defamation of character as well as carrying out the necessary due diligence as enshrined in the Nigeria Data Protection Regulations."

What this means: Those pesky messages loan companies send to your contacts can now be reported to NITDA. In fact, I'm pretty sure that a class action lawsuit can come out of this. Please sue these silly companies from here to Highwater.

Speaking of suing companies, who is going to sue the CBN for illegal loans it keeps extending to the federal government? Any takers?

The Ways and Means of a hefty loan

Let's establish a few things:

The CBN is allowed to finance the FG's fiscal deficit a.k.a borrow the government money through what experts call Ways and Means Advances

The CBN can only borrow the government 5% of the government's previous year's revenue - anything else is unconstitutional

Those loans must be repaid within the same year

Between 2015 and 2020, the total lending to the FG was ₦11.0tn when it should have not been more than ₦491.3bn

Ways and Means Advances have ballooned to ₦15.51tn, rising by %2,286 in six years

The ₦15.51 Trillion the FG owes to CBN is not part of the country’s total debt which was ₦33.1 Trillion as of March 2021.

While the CBN has these very real problems to deal with, there’s also some important conversations that need to be had.

It’s time for digital banks to have their own licences

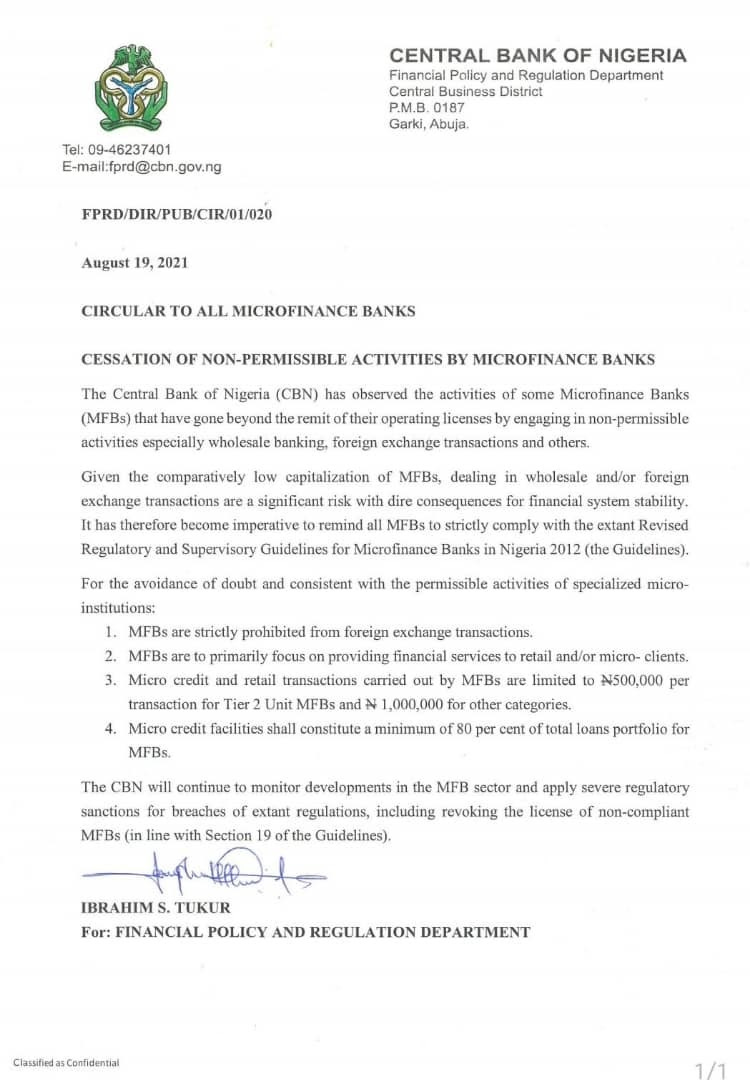

Nigerians on Twitter were immediately suspicious when the CBN’s new circular reminded microfinance banks of the limits of their operations. Part of the memo reads, “The CBN has observed the activities of some Microfinance Banks that have gone beyond the remit of their operating licences by engaging in non-permissible activities especially wholesale banking, forex and others.”

As some Twitter users pointed out, digital banks like Kuda and VFD use Microfinance bank licences to operate. Yet, digital banks are not what microfinance bank licences were created for, and regulation has not caught up with how big and important some of these digital players have become. PiggyVest for instance said it paid back ₦90 billion to customers last year.

So, while the microfinance bank licences have become the easy fix for digital banks, it is high time the CBN started working on a framework for digital banks. The need for a licence category is of course because microfinance banks are supposed to be focused on financial inclusion and reducing poverty by giving microloans. There’s also no way these digital players can pay for commercial bank licences which cost ₦25 billion.

I doubt this memo will catch digital banks by surprise, the CBN has spoken about raising the capital requirements for microfinance banks for over a year now. I know regulations are often seen as a bad thing in Nigeria, but this time, they are actually super necessary.

That’s enough reporting for one day, here’s what I read all week.

What else I’m reading:

In a more balanced and nuanced reporting on Nigeria’s fintech sector, the Financial Times actually does some great work here.

Some of the most brilliant reporting on Nigeria’s plan to lure top Boko Haram defectors was done by Obi Anyadike; it is as carefully done as it is disturbing

As though it were not already neck-deep in debt, Nigeria is planning its first tranche of a $6.2 billion Eurobond

Abubakar does the business in this Rest Of World article about how regulatory clampdowns in Nigeria is making everyone jittery is pretty good

NO AUDIO LOVE - SHARE NOTADEEPDIVE

I get a lot of mentions and direct messages on social media telling me how much you love the newsletter, but it’s not translating unless you share it. Please take some time to share the newsletter today if you enjoy it and be sure to leave a comment.

What am I doing this Friday you ask? Holing up at home and recovering from a health scare, while my doctor is judging me for doing any sort of work at all. There’s no beer in the near future for me, so be sure to drink a bottle or two for me.

I’m taking Sunday off - I mean it this time - so see you next week!

* The legal analysis of the CBN’s ex parte motion against fintech startups was done by Lily Odunaiya, you can subscribe to her newsletter on law and technology, Techgavel, here.

I believe that at some point, these coys should test these things in court. This constant bullying by the apex bank is not only terrible for the ecosystem but detrimental to the nation in the long run. It is about time the Tech community stand up to these bullies.

I really do enjoy reading your newsletters, Chief. Thanks a lot for writing them.

I'd have loved it if you had written more on the FG vs MFBs regulations ish. It was interesting, but short.

Thanks once again, sir.