Canal+ Was Always Going to Kill Showmax

Forget data costs and African consumers. The answer is in a French investor presentation from January.

If you missed last week’s Notadeepdive, catch up here and here. If this newsletter was forwarded to you, subscribe here for free:

TOGETHER WITH CREDIT DIRECT

The tax reforms have been passed. How prepared are you? March 31 is the filing deadline for employed individuals. June 30 is the corporate deadline for business owners. Both are closer than they feel right now.

Our Head of Finance and Strategy, Dr. Emeka Ucheaga, sat down with Abiodun Kayode-Alli, Senior Tax Consultant at PwC, for a conversation that cuts through the noise, what the new reforms actually mean, what they change for your business, and what you should be doing before the deadline arrives.

Canal+ Was Always Going to Kill Showmax

In February 2024, I was in Johannesburg for the launch of Showmax 2.0, a black-tie event that was a masterclass in branding.

The gist of the launch was that MultiChoice was finally ditching its aging in-house tech, after writing off $65 million on a failed technology modernization project, to jump into bed with Comcast’s NBCUniversal.

With Showmax 2.0, the continent was getting a streaming service with Peacock’s world-class tech, a deep library of local content, a pipeline of HBO and Universal content, and the crown jewel that is the English Premier League on mobile for a subscription price that undercut the global streamers. The target was 50 million subscribers and $1 billion in revenue in five years.

“[It is] the beginning of what the company hopes will be a long march into dominating and making a solid business of African video streaming,” I wrote at the time.

That long march has now been truncated. On March 5, 2026, MultiChoice sent that email to customers. “The Showmax Board has taken the decision to discontinue the Showmax service in the near future,” part of that email said.

All said, Showmax 2.0 lasted two years.

The immediate reaction was that streaming doesn’t work in Africa, data costs are too high, and consumers can’t pay. None of that is wrong, and there’s already a good analysis of those factors. But the more interesting story is about two business models that were never going to coexist and about how anyone who understood Canal+ could have predicted this outcome the moment it crossed the 35% ownership threshold in MultiChoice.

Canal+ was always going to kill Showmax.

How MultiChoice arrived at streaming

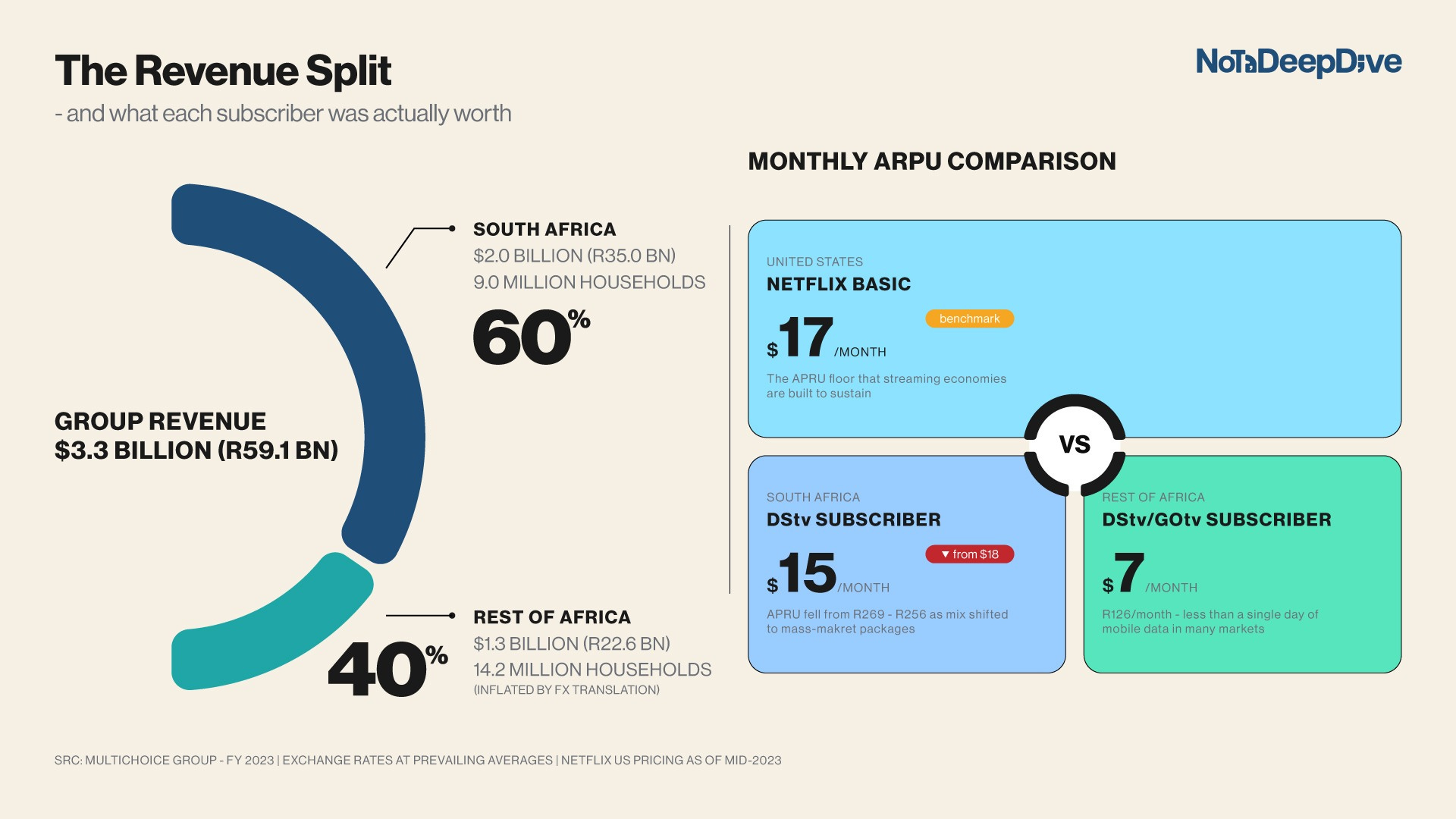

MultiChoice’s pay-TV business appeared to have peaked in 2023. For the South African business, stage 4 of loadshedding caused considerable churn, even among customers with disposable income. By FY25, Zambia, Zimbabwe, and Malawi were experiencing severe power shortages.

Meanwhile, paying Showmax subscribers grew 68% year-on-year in FY22. Showmax Pro (the tier with live sports) doubled its subscriber base in FY23. At various points, Showmax reportedly had more subscribers than Netflix across sub-Saharan Africa.

It was easy to interpret it as part of a global trend of cable and satellite TV losing market share to streaming. MultiChoice’s customers were migrating from dishes to screens, the thesis went, and the question was whether MultiChoice would own that future or be disrupted by it.

MultiChoice had content — 91,470 hours of it in more than 45 languages — a SuperSports rights portfolio spanning the EPL, Champions League, and LaLiga, and was operating in 50 African countries. The feeling was that dominance would be inevitable once it had the right technology.

The Vice: Assumptions vs. Hard Reality

In FY2024, Showmax’s trading losses stood at $141 million on revenue of $55m. In FY2025, losses ballooned to $274 million on revenue of $42m. Showmax was spending more than $6 for every $1 it brought in.

The relaunch alone cost approximately $180 million, including $91 million to customise Peacock’s tech for Africa. It also paid quarterly licensing fees to Comcast. In FY24, NBCU exercised its contractual right to sell its 30% Showmax stake back at a predetermined price of $160 million. Canal+ is now writing down $85 million to dissolve the relationship entirely.

Showmax, which accounted for roughly 2% of group revenue, wiped out nearly half the group’s profitability in FY25.

MultiChoice was now losing on two fronts.

In March 2025, MultiChoice lost 2.8 million linear subscribers. Nigeria, which once drove 44% of Rest of Africa revenue, was hit with FX volatility and inflation. MultiChoice’s Rest of Africa revenues fell 44% in dollar terms with a trading loss of R760 million on a reported basis. The segment that had finally turned profitable in FY23 was back in the red within two years.

So MultiChoice was caught in a vice. The old business was shrinking. The new business was hemorrhaging cash, and the macroeconomic environment was actively destroying both.

Canal+ was never going to keep Showmax

Canal+ is not a standalone streaming platform and has never been one. Understanding this is the key to understanding why the Showmax shutdown wasn’t a reaction to bad results. It was baked into Canal+’s business model from the beginning.

Canal+ launched myCanal in December 2013 as a streaming app for its French subscribers. But the platform was designed as an aggregator with one interface through which subscribers could access Canal+’s own channels and third-party services.

By 2019, Canal+ had bundled Netflix into its French subscription tiers. By 2020, Disney+ was included for Ciné Séries subscribers on launch day. Paramount+ and Max followed. Apple TV+ came in 2023.

Canal+ CEO Maxime Saada has described the company’s relationship with Netflix as “80% partners and maybe 20% competitors.” He credited Netflix with doubling France’s paid television market, growing penetration from 30% to 75%. This is not a company that views Netflix as the enemy.

The Canal+ model is basically to avoid competition with global streamers but aggregate them instead. You’ll take a margin on distribution and layer in your own premium channels and local content on top. All the while, you own the customer relationship.

Showmax’s model was to compete directly with Netflix, Amazon, and Disney+ for subscribers and content. It built a proprietary content pipeline and licensed expensive third-party content from HBO, Warner Bros, and Sony.

These two models are structurally incompatible. You cannot simultaneously compete with Netflix (Showmax) and bundle Netflix (Canal+). You have to pick one.

Canal+ picked its model decades ago, and it has already demonstrated how it deploys this model in Africa.

In Francophone Africa, where Canal+ has operated for more than 30 years across 19 countries, it runs the Canal+ app with local and international content aggregated through a single subscription. In June 2025, just months after completing the MultiChoice acquisition, Canal+ struck a strategic Netflix bundling deal for 24 sub-Saharan Francophone African countries. Canal+ became the first operator to bundle Netflix subscriptions into traditional pay-TV offerings across the region.

The NBCU partnership made the structural incompatibility worse. The joint venture gave Comcast — a company with no strategic alignment with Canal+ — a 30% equity stake in MultiChoice’s streaming asset, ongoing licensing fees, and embedded cost structures that Canal+ couldn’t control. Canal+ was subsidising a third party’s position inside its own newly acquired business.

Then there’s the math. Canal+ acquired MultiChoice at R125 ($18) per share, valuing the group at approximately R35 billion ($2 billion). To justify that premium to its own investors, Canal+ committed to delivering R7.5 billion ($417m) in annual cost synergies from the combined group.

That’s just corporate speak for finding money. The single fastest way to find R7.5 billion in a business is to stop spending $272 million a year on a loss-making streaming service.

Saada was blunt about it. In January 2026, he told investors Showmax was “not a commercial success; it’s quite obvious.”

CFO Amandine Ferré added that the losses were “not acceptable.” David Mignot, the new MultiChoice Group CEO appointed by Canal+, told TechCentral just two weeks before the shutdown that Showmax “can’t continue” in its current form. His exact words: “Financially speaking, business-wise speaking, the thing is not flying.”

Canal+ had been in control for less than six months when it finally pulled the trigger.

Calvo Mawela stood on that stage in Johannesburg and described the beginning of a long march. He was right about the march. He was wrong about the direction.

See you on Sunday!

Numbers are stubborn! That Canal+ could reverse the then impending exit of CNN etc from DSTV shows the depth of capabilities they posses. Multichoice was right with Showmax back then, Canal+ is right regarding shutting down Showmax now.

The benefit of hindsight is 50/50

This is the most comprehensive article and defies all rumors about failure of streaming in Africa. Thanks a bunch