Customer accepted higher tariffs, telcos now need to suck it up

Will customer compensations improve network quality?

Happy Manchester City beat Chealsea day to all who celebrate.

If you missed Friday’s newsletter, catch up here. If this newsletter was forwarded to you, subscribe for free:

TOGETHER WITH CREDIT DIRECT

The question business owners need to start asking is “How do I keep more of the money my business is making?”

Credit Direct has partnered with Mr Olagoke Balogun to answer this question.

Join us on the 18th of April for a virtual session on Money Talks: The Cash Flow Blueprint for Building 100M+ Businesses.

Customer accepted higher tariffs, telcos now need to suck it up

Typically, when your network is bad in Nigeria, you can swear at your telecom provider, type an angry complaint on social media using the same bad network, and well…move on with your life. Starting this month, the Nigerian Communications Commission says the networks should feel some of that pain too. Under a new framework, subscribers in areas affected by poor service will receive automatic airtime credits. The operator will identify the affected local government area, match it against subscribers who actually generated billed usage there, and issue credits to affected users.

A heavy data user with a miserable connection should therefore get more than a light caller, because the credit is tied to usage and spending patterns. The cost to the operator rises with the revenue it is earning from the people and places it is underserving.

Earlier this year, TechCabal reported that the regulator was moving to impose about ₦12.4 billion in penalties across the industry for breaches of service standards. That sounds severe until you compare it to the scale of the business. MTN Nigeria alone reported ₦5.2 trillion in service revenue and ₦1.1 trillion in profit after tax.

Nigeria has tried compensation before. In 2008, Ernest Ndukwe’s NCC ordered MTN and Celtel to compensate subscribers for persistent poor quality. The operators resisted the whole thing, went to court and lost. MTN later moved to refund about ₦2.7 billion in airtime, and Celtel rolled out a phased compensation plan.

Today, the operators’ best defence is that the new compensation framework attacks the symptom, not the cause. They will point to fibre cuts, diesel costs, vandalism, and the ugly economics of rolling out infrastructure outside the richest corridors. Some of that is true.

But customers also accepted higher tariff prices, and the largest operator is back to profitability. The harder it becomes to argue poverty, the easier it becomes for the regulator to argue that bad service should cost money.

More Lending Is Easy

In June 2023, the Tinubu administration and the CBN got sick of kicking the can down the road and decided to let currency prices be decided by the market. If policymakers took forever to get to a common-sense decision, Nigeria’s big banks had been around long enough to position themselves to profit from a currency repricing.

By December 2024, Zenith held ₦281 billion in derivative assets — the unrealised gains on those positions — against ₦9 billion in derivative liabilities. 2024 rewarded banks for surviving a huge currency repricing.

A year later, those gains went the other way and derivative assets were ₦8 billion vs derivative liabilities of ₦196 billion. Everyone had to go back to the less glamorous business of being Nigerian banks, which, as I pointed out two weeks ago, is less about lending and more about smart capital allocation.

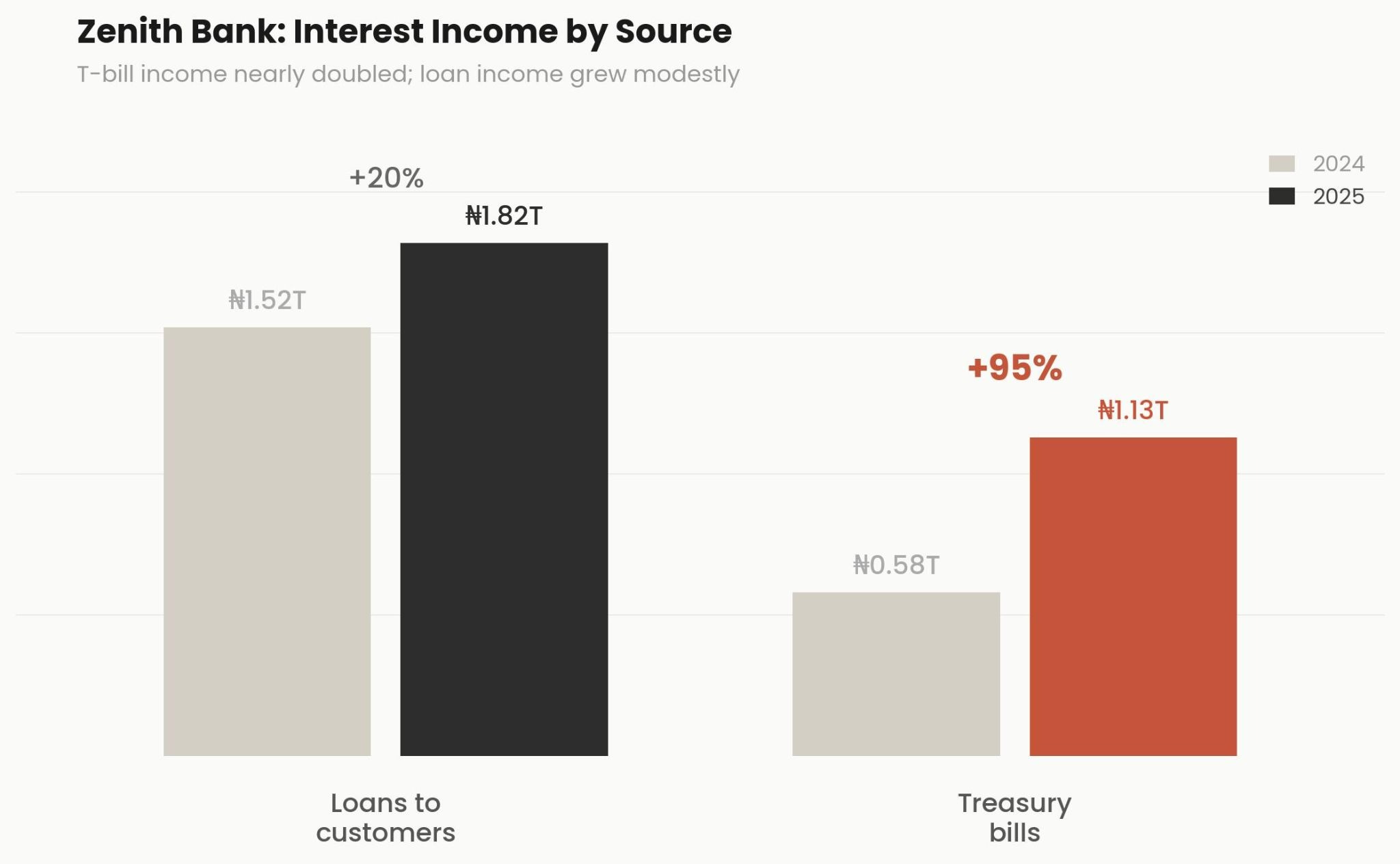

Consumer lending was ₦180.6 billion, down from ₦336.5 billion the year before. It is even smaller than GTCO’s retail lending bucket, which was ₦249.2 billion in 2025. If there’s a retail lending party, Zenith Bank is happy to stay at home. Instead, it piled money into treasury bills, pretty much risk-free and called it a day.

Bonus: Zenith wrote off ₦1.24 trillion of loans in 2025 and framed it as a “bold and prudent clean up.” The reality was more like it was a forced clean-up after the CBN stopped letting banks avoid full provisioning on some stressed foreign-currency loans. It was decided that banks under the forbearance regime could not pay dividends, bonuses to directors and senior management, or invest in foreign subsidiaries until their capital and provisioning positions were fixed.

That said, Zenith remains a deposit-mobilising monster with total deposits reaching ₦24.33 trillion. It has 30 million cardholders and 456 branches.

See you next week!