Eden Life vs. Arithmetic

Great idea. Brutal macros. Unit economics wins this round

If you missed Friday’s Notadeepdive, catch up here. If this newsletter was forwarded to you, subscribe here for free:

Notadeepdive is powered by two super supportive brand partners, Credit Direct and Busha. Make sure to check them out!

TOGETHER WITH CREDIT DIRECT

Generosity is great, but strategic generosity changes lives. Gift A Yield transforms your kind gesture into a compounding investment.

By gifting a Yield plan to someone, you aren’t just giving money; you’re giving them a future they can actually use. While other gifts lose value, a Yield plan compounds. It’s strategic, it’s thoughtful, and it’s the only gift that literally pays them back. Give them a financial head start today.

A great consumer idea loses the fight with unit economics

A few weeks ago, Eden Life’s founder got out ahead of a brewing story about the company’s future. We now have the version with context, and we’ll take it.

Eden Life has now clarified that it’s not shutting down, but making a “strategic transition.” The corporate-speak continues: “We are temporarily de-prioritising our individual consumer (B2C) offerings to consolidate our resources and focus on our high-growth, profitable B2B market.”

The company says its industrial catering and corporate food subscriptions, which it calls “primary growth drivers,” will continue.

This is not a dunk on anyone. Startups are hard, and half the time, they’re trying to conjure from thin air stuff that didn’t exist before. In Eden Life’s case, what they initially built looked like a concierge service: offering Nigeria’s busy working-class the chance to get chef-cooked meals, sort out laundry, and handle home cleaning through trained professionals.

If you’re the kind of person who’s busy enough to use Chowdeck, Glovo and FoodCourt more than 100 times a year, you eventually hit decision fatigue: too many menus, too many choices, only to still end up ordering the same three things. And if like me, you work on weekends, you want someone to come in and do the cleaning and laundry. When you think about it, it was quite a solid idea.

A few of my friends used it after it launched, and I could see how it would play well with the upper middle class as a soft bit of convenience and a status signal (not a bad thing!).

Yet, I wasn’t convinced that the idea would reach critical mass (to be fair, I’ve been known to take the dim view on many things). There was also the small matter of being a poor journalist, so I wasn’t the target market. However, my skepticism was based on something more structural: unskilled/semi-skilled labour is pretty cheap in Nigeria.

Eden Life was up against restaurants, laundromats and a bunch of other businesses, but on some level, it was up against the real alternative: cheap labour. It’s the same reason platforms for aggregating quality/professional artisans haven’t become wild successes (VConnect worked on this for years).

The pitch for a platform like Eden Life is that you’re paying for reliability: trained professionals who won’t waste your time or do a shoddy job. What Eden tried to do was to make a product out of the experience: vetting, training, punctuality, replacements, QA, and customer support. That predictability is the product, but it’s also expensive to deliver.

Compare that to cheap labour. You can hire a mediocre artisan or a live-in cook who cuts corners here and there because firing them and hiring a replacement is easy. So the high cost of “professional and reliable” has to compete with “cheap and good enough,” and cheap-and-good-enough is a brutal competitor.

You also have to factor in Nigeria’s worsening macro environment at the time.

Nigeria’s food inflation hit 40.87% YoY in June 2024 (with headline inflation at 34.19% YoY that same month). It meant inputs get more expensive (ingredients, diesel, packaging, labour expectations). When your customer’s discretionary budget shrinks, they reclassify convenience as a luxury.

Eden got creative, using laundry as the on-ramp to upsell meals. But the fight with the unit economics would have been very tricky. We don’t have their numbers, so we have to get creative.

In 2023, TechCabal reported Eden raised subscription pricing to ₦150,000 for two meals daily. So for 60 meals a month, that’s ₦2,500 per meal in revenue.

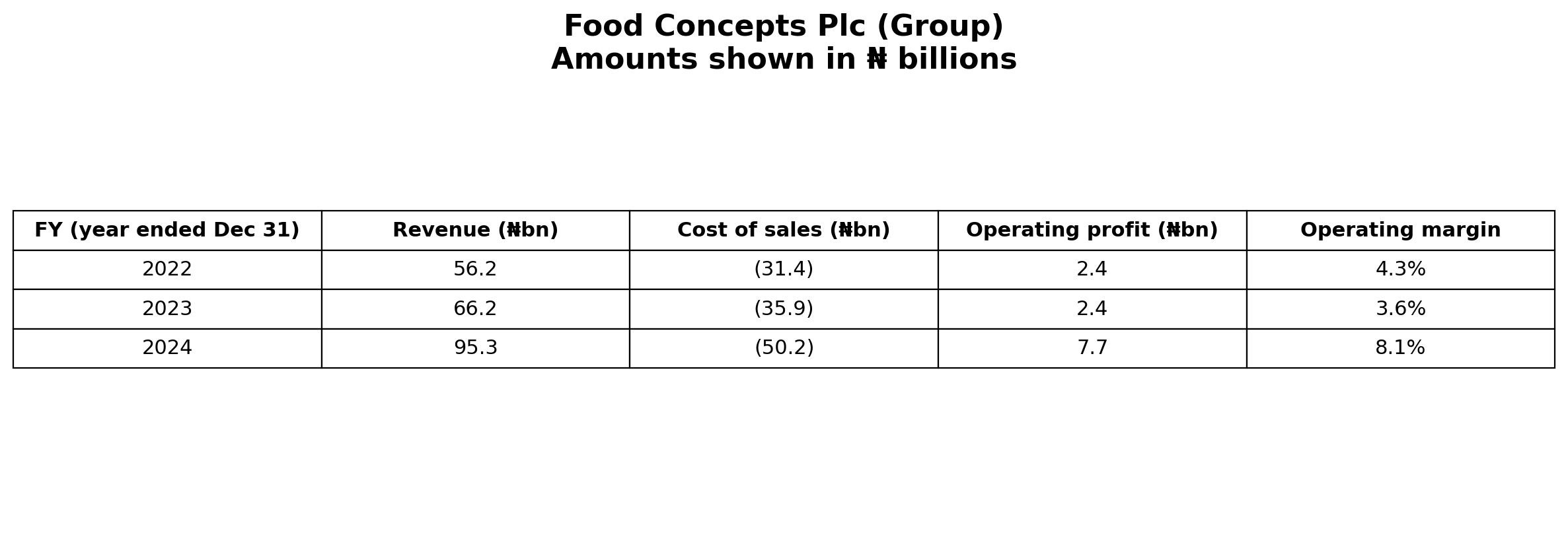

Big Quick Service Restaurant operators spend ~50% of revenue on raw materials. Food Concepts Plc reported raw materials/consumables of ₦50.157bn on ₦95.250bn revenue in 2024 (~53%).

Eden is smaller, offers premium, and deals with more variability, so it’s safe to assume raw materials took 55–70% of revenue, something like ₦1,375–₦1,750 per meal. Packaging would be something like ₦150–₦300 per meal (containers, branding, cutlery, sealing).

You also have to deliver the items. Even if the customer pays for the delivery, you have to manage the operations and scheduling. There will be wrong addresses, customers not picking up phones, having to make the same delivery twice, etc.

If we extend our back-of-the-napkin analysis, we could assume:

Revenue: ₦150,000

Raw materials (say 60%): ₦90,000

Packaging (₦200 × 60): ₦12,000

Delivery + ops: ₦15,000–₦30,000

Kitchen labour / QA overhead allocation: ₦15,000–₦25,000

That’s ₦132,000–₦157,000 before paying for customer support, refunds, marketing, tech, management, rent, and sundry infrastructure.

Eden soon bolted on a quick service restaurant (QSR) model, listing meals on food delivery apps. But QSR models are engineered for volume because the margins are thin even for established players.

Look at Food Concepts Plc, the group behind Chicken Republic:

Even in 2024, which was a good year for Food Concepts, likely helped by pricing power and naira effects, you’re still looking at single-digit operating margins. That’s with the scale and brand recognition of Chicken Republic behind you. For a startup trying to bolt a QSR model onto an existing concierge play, you can only imagine what the math looks like.

Ultimately, Eden Life couldn’t wrangle positive unit economics serving individual customers as macroeconomic conditions deteriorated. It’s tempting to imagine how this business would have fared with a stronger economy and a larger, more stable upper middle class. But here’s where we are. I wish them luck in the more profitable but 60-day payment cycle world of B2B.

TOGETHER WITH BUSHA

If you are a business exploring digital assets for cross-border payments or treasury management, you should check out Busha Business. Busha business also allows you to buy, sell, receive, and send stablecoins and digital assets.

How much room does the Nigerian household actually have?

In partnership with Risevest

Speaking of inflation squeezing consumers out of things they used to afford, Risevest published its 2025 Cost of Living Report last week, and the numbers put some flesh on the bones of what we’ve been discussing.

The headline finding won’t surprise anyone who’s been paying attention: the macro is improving, but households aren’t feeling it yet. Nigeria’s inflation eased to 18% by September 2025, and we even got our first month-on-month food price decline in over 13 years. A 50kg bag of rice that cost around ₦90,000 in mid-2024 fell to roughly ₦57,000 by October. On paper, it’s real progress.

The survey puts the average Nigerian income at ₦467,268 a month, but that number is puffed up by a small number of high earners. The median, which better reflects what a typical person actually takes home, is ₦200,225. About $125 a month. That’s the reality for most.

Against that, 62% of respondents spend more than 60% of their income every month. One in six spend more than they earn, plugging the gap with savings, borrowing, or informal credit. The estimated cost of living for a family of four in Lagos — excluding rent — is ₦1.24 million monthly, so you start to understand why.

And the cost pressures come from everywhere. Rent surged over 80% in parts of Lagos over the past year. Band A electricity tariffs more than tripled. Fuel sits above ₦950 per litre, which flows into everything from transport to the price of tomatoes. Healthcare costs doubled year-on-year. Each of these individually is manageable for a high earner. Stacked together against a median income of ₦200,000, the arithmetic is brutal.

The one encouraging finding: Nigerians are saving more. The average savings rate jumped from 15% to 21.5%, the sharpest improvement across all four countries surveyed. As food inflation eased, it freed up money that was previously going straight to rice and garri. But it also reflects a population that went through the worst of 2024’s inflation crisis and came out with more defensive habits. People are buying in bulk, cutting non-essentials, and putting money aside with real discipline.

85% of respondents are actively investing in something, with real estate, stocks, and mutual funds leading the pack. The shift toward dollar-denominated assets and digital investment platforms is pronounced — unsurprising when your local currency has lost the kind of value the naira has over the past three years.

The full report covers four countries across 118 pages and is worth reading if you care about how African households are actually navigating this economy — not the macro version, the lived one.

See you next week!

If you liked this newsletter, please share and like!

Hi. Objection the man is trying to evade the new tax laws by cosplaying again as a starving writer. He's rich your honour.

This country is too poor. Ugh.