Everyone wants to know about Jumia’s timeline

How Jumia went Left

Welcome to the 150 people who joined Notadeepdive last week. If you’re new here, leave a comment below. I’ll pick two new subscribers at random and send them some Notadeepdive merch.

And to OGs, last week’s Notadeepdive was our most-read newsletter ever, but you might have missed it. Check your Promotions or spam folder and, if it landed there, drag it back into Primary so the next one reaches you properly.

As always, if this email was forwarded to you, subscribe for free:

TOGETHER WITH CREDIT DIRECT

The conference about money just got a sponsor that understands it.

Yield by Credit Direct is headlining Naira Life 2026, Zikoko’s annual gathering for Nigerians who take their financial lives seriously.

August 22nd. See you there!

Everyone wants to know about Jumia’s timeline

If I were into “prediction markets” a.k.a betting apps with extra steps, one sure-fire wager is that every time a journalist asks me for a comment, the company they want answers about is Jumia.

“When will Jumia become profitable?” is a favourite question.

“Can it beat Chinese competitors like Temu and Shein?” is another.

These are useful questions, but they are too focused on what Jumia is doing now when much of the answer is buried in its past.

Francis Dufay took over from co-CEOs Jeremy Hodara and Sacha Poignonnec in November 2022. And like several Jumia leaders before him, he arrived promising greater discipline and a credible path to profitability.

By the end of 2020, Hodara and Poignonnec said Jumia had been put “firmly” on track towards breakeven. Marketing spend had fallen, costs were being cut, and the company’s adjusted EBITDA loss was shrinking.

Then Jumia’s share price climbed to an all-time closing high of $65.51 in February 2021. The company sensibly took advantage of the excitement, raising $341.2 million from investors in March. This came only four months after another share sale had raised $231.4 million. In total, Jumia raised $573 million in new money.

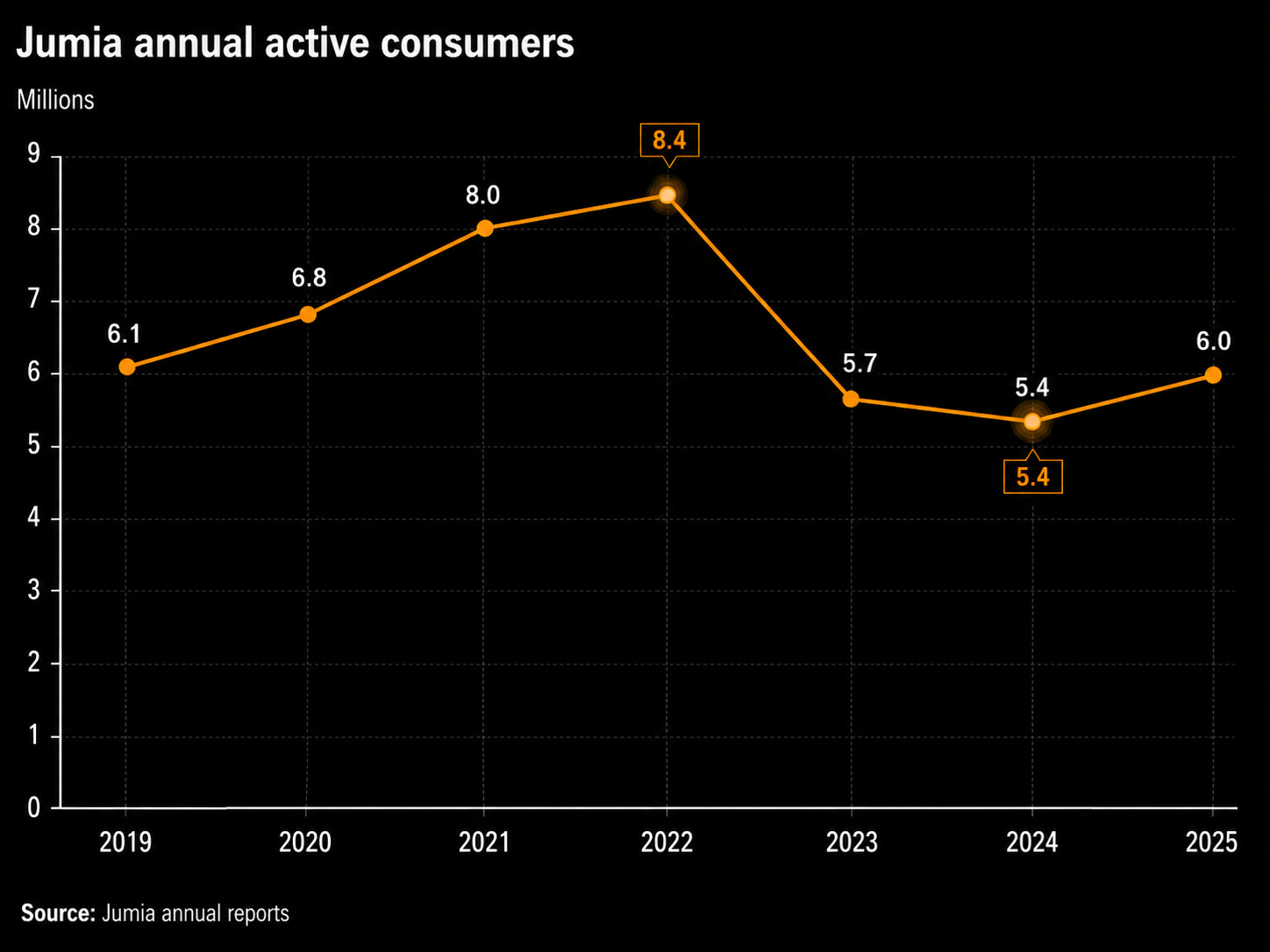

Now flush with cash, sales and advertising spending more than doubled, rising from $37.1 million in 2020 to $81.9 million in 2021. Annual active consumers grew by 18%, from 6.8 million to 8 million. But operating loss widened 41% to $240.9 million.

The spending continued into 2022 with another $75.7 million on sales and advertising, while its adjusted EBITDA loss reached $207 million. Hodara and Poignonnec left that November.

There is a pattern here of Jumia becoming disciplined when its back is against the wall. When money is scarce, it cuts employees, closes businesses, exits markets and discovers efficiency. When money is abundant, it has historically found new ways to spend it.

That is the context in which Dufay’s latest profitability promise should be understood.

For now, Jumia is walking the talk. Its headcount has fallen from 4,318 employees at the end of 2022 to just over 1,980 in March 2026. In the first quarter of 2026, GMV grew by 32% after adjusting for exited markets, physical-goods orders grew by 31% and adjusted EBITDA loss fell by 32% to $10.7 million.

Jumia now says it will reach adjusted EBITDA breakeven and positive cash flow in the fourth quarter of 2026, before delivering full-year profitability and positive cash flow in 2027.

The real test is not simply whether Dufay can enforce discipline while Jumia has limited cash. It is whether the discipline survives success. What happens if the share price rises again and management is given room to become ambitious?

There is also a more fundamental question: has Jumia actually expanded the market for online shopping, or has it mostly bought temporary bursts of activity?

In a November 2014 TechCabal article (one of the many gems I found in my research), Feyi Fawehinmi described African ecommerce as “a tough business that is not for the faint of heart.” At the time, only 360,000 people had bought something from Jumia. Nigeria had roughly 170 million people, internet adoption was growing, and yet the appeal of shopping online remained limited.

Jumia has obviously grown since then, partly powered by an extraordinary amount of investor money. But customer growth peaked in 2021 and has trended downwards even as more Nigerians shop online.

Of course it’s worth mentioning that Jumia has exited countries, closed businesses and changed the mix of activity counted on its platform.

Still, the broader question remains. Historically, whenever Jumia placed discipline ahead of expansion, growth slowed. Dufay must prove that discipline can produce efficient growth rather than simply manage decline.

This is why Jumia’s story needs more than a short article or a quick quote to a journalist. Like the story we published last week about Nigeria’s 2008 stock-market crash, it rewards going backwards, following the money and examining the gap between what people said and what they actually did.

But it also demands a different format. So we made a podcast.

A few weeks ago, I shared the first episode of our Jumia series. About 200 people clicked through and listened. Episode two is now out, and I genuinely think it is worth every minute of your time.

You can listen on YouTube, Spotify, Apple Podcasts or Deezer.

We are going to do much more long-form work over the next year, and your feedback will be essential to what this becomes. It would be fantastic to get this episode to 2,000 listens.

Please listen. And if you enjoy it, give the show a rating, like the episode, or share it with someone who has ever wondered how Jumia managed to spend so much money without becoming profitable.

And if there’s something you hate, your feedback will help make this much better.

It is really entertaining stuff, if I say so myself.

Well, I got the mail and…, I'm here for the merch.

But wait, is Jumia listed on the NGX???