Food Delivery’s Battle for Nearness

FoodCourt, Food Concepts, food delivery....physical location in five.

I don’t write about Nollywood often, so if you missed it, catch up here. If this Notadeepdive edition was forwarded to you, subscribe here for free:

TOGETHER WITH CREDIT DIRECT

Get the most powerful vivo phone with just a 20% down payment. Use Credit Direct Checkout, the smarter way to shop.

The proximity business of food delivery

In Lagos, food is the cheap part (relative to inflation!); there is white rice or jollof rice on every street. Shawarma, mediocre spaghetti, and turkey are usually two stalls away on busy streets. The economy may have thinned out bukkas because rent is insane, but a hungry person in Lagos is never really far from a meal.

So when you use a food delivery app, what you’re paying a premium for is the nearest good meal the moment you decide to eat, brought straight to your door.

Inevitably, everything in food delivery is a contest over who supplies nearness to the customer, and in the fine print are questions like, “At what cost?” or “Who paid to create the demand in the first place?”

Restaurants, delivery apps, and cloud kitchens are three answers to the same question.

What prompted these thoughts around food delivery is FoodCourt. Since March, FoodCourt has been unavailable on Lagos Island. When customers asked whether it had shut down, the company said its Lekki hub was briefly offline for “operational adjustments.”

That adjustment appears to have now spread to the mainland. On the FoodCourt app, pretty much all items are unavailable, and on Chowdeck, where it was listed for ages, it’s no longer there.

This is not the YC-backed startup’s first wobble. Foodcourt undertook an operational overhaul and cut nearly 100 staff in 2024, and if you think about it, the startup was built to win the market in a specific way.

How do you win the battle for nearness to the customer?

The restaurant has the cheapest answer. A Chicken Republic on a busy road sells meals for rent it will pay anyway. The staff works in shifts, and people walk in for breakfast, lunch, and dinner. The physical space is for cooking and dining, but it also advertises the space, generating demand from existing foot traffic. Customers don’t have to be acquired in that sense.

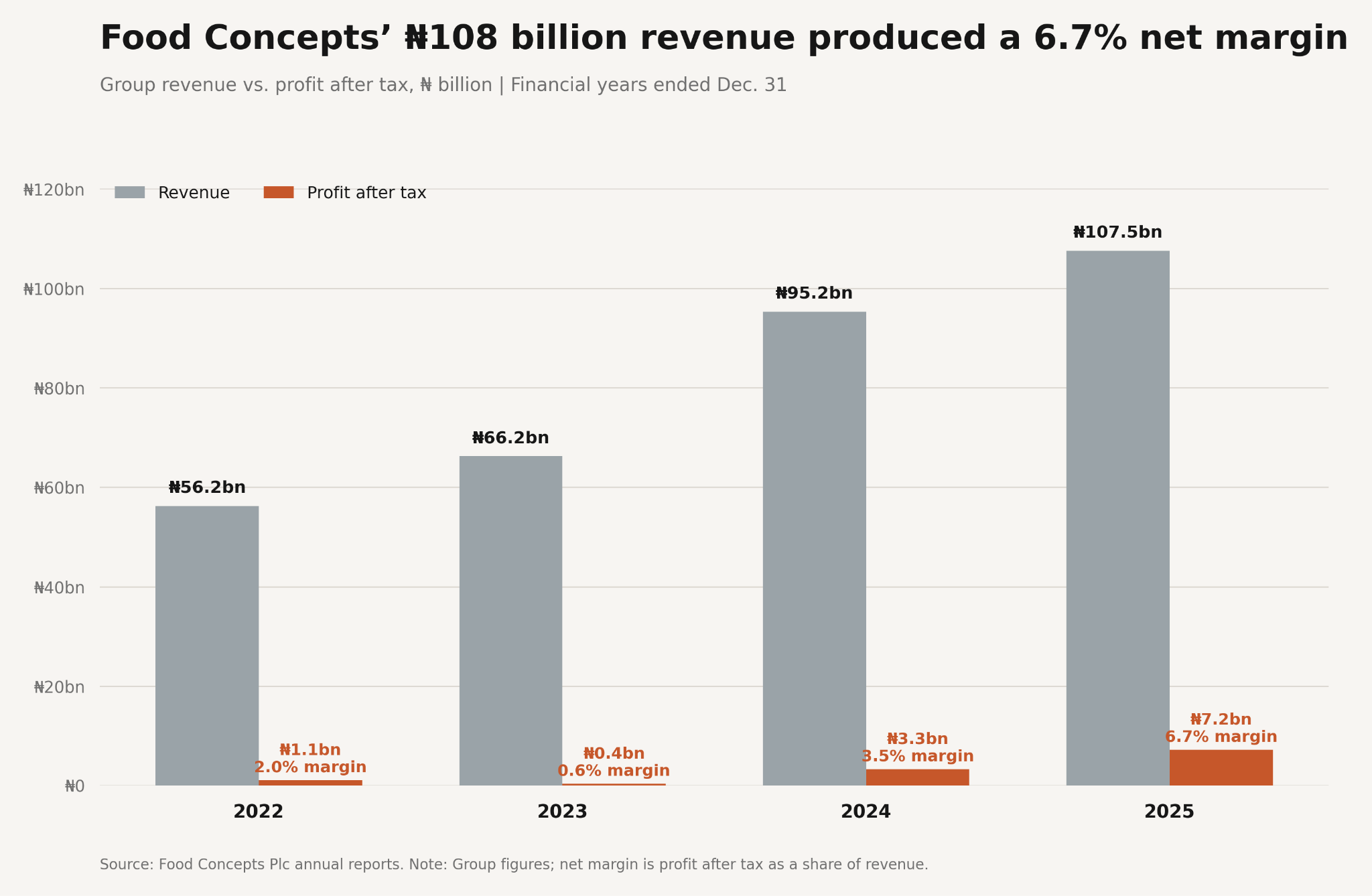

Food Concepts, the company behind Chicken Republic, PieXpress, and Chop Box, makes most of its sales from walk-ins. In 2025, its restaurants brought in ₦106.8 billion of the group’s ₦107.5 billion in revenue.

It made ₦7.2 billion of profit after tax which meant it kept seven kobo kept for every naira earned. And that’s the entity with the “cheapest” nearness to the customer. In 2023 the company kept ₦377 million on ₦66 billion — six-tenths of one kobo — after a falling naira and a ₦5.5 billion diesel bill.

The delivery app is the expensive answer to proximity to customers. It doesn’t have kitchens, so to offer proximity, it invests in infrastructure like logistics, inventory management, technology, etc. After the restaurant takes the food margin and the rider takes the trip, what reaches the platform is a sliver, and out of that sliver come refunds, promotions, and technology costs.

How thin is that sliver? DoorDash, with tens of millions of repeat users and a thriving subscription business, completed 903 million orders in Q4 2025 worth $29.7 billion and eked out a profit of $213 million.

Measured against the food that moved through the platform, that’s seven-tenths of a cent on the dollar, after a decade of operations and real scale. In Nigeria, Jumia, which had every reason to make it work, shut Jumia Food across seven markets in 2023 and said it had never been profitable. Bolt Food left the same year. Engineering proximity to the customer is a worse business than owning it.

So here’s an idea. Why not be both and double your odds? Own a dozen virtual brands (FoodCourt’s Chinese menu is good), cook your food in centralized kitchens, sell directly to customers, and skip paying commission to food delivery companies.

To be both, the cloud kitchen has to remove the dining space, because that’s the expensive part. But the space doubled as a billboard of sorts. If you take it away, the rent for premium space disappears, but in its place, you’ll pay to acquire every customer who would otherwise have walked in. Every order will now begin with someone installing an app.

Realistically, alongside the app, you’ll likely need to list on a bigger platform like Chowdeck anyway and pay commission. You might even have to pay some advertising fees for premium placement and then pay a commission anyway.

Cooking a dozen menus to order from one space is slow, and orders will run late (in my experience, you should eat two small noodles before you order). It forced FoodCourt to rebuild the kitchen in 2024 and start cooking base ingredients ahead of demand. It also cut staff. The shared kitchen that saved on rent was not immediately as efficient as thought.

This is not a Nigerian failure of nerve. FoodCourt’s closest analogue is Rebel Foods in India — the same model, multiple virtual brands from shared kitchens ordered through its EatSure app, scaled past 45 brands across 80 cities. In the year to March 2025, Rebel made about $191 million in operating revenue and lost nearly $40 million, spending $1.23 for every dollar it earned. It now runs 19 offline stores and pitches franchisees a 1,500-square-foot outlet with a dine-in Oven Story pizza store out front and cloud kitchens behind it. Elsewhere, the same retreat: Kitchen United fell back to selling software, and Kitopi rebranded as a hospitality company with more than 200 physical outlets across the Gulf. Nobody stayed with the pure cloud kitchen for long.

This is not a uniquely Nigerian problem. FoodCourt’s comparable is Rebel Foods in India. They have the same model of multiple virtual brands from shared kitchens ordered through its EatSure app, scaled past 45 brands across 80 cities.

In the year to March 2025, Rebel made about $191 million in operating revenue and lost nearly $40 million, spending $1.23 for every dollar it earned. It now runs 19 offline stores and pitches franchisees a 1,500-square-foot outlet with a dine-in Oven Story pizza store out front and cloud kitchens behind it.

Elsewhere, the same retreat: Kitchen United pivoted to selling software, and Kitopi rebranded as a hospitality company with more than 200 physical outlets across the Gulf. Nobody stayed with the pure cloud kitchen for long.

Let’s turn back to Chicken Republic, which offers the cheap version of proximity at 190 locations, where delivery is a layer on a kitchen a walk-in crowd already pays for. Food Concepts’ receivables note shows ₦12.632 billion of additions and ₦12.228 billion of collections during 2025. The company says those movements included e-commerce sales through Glovo and Chowdeck.

Its size means it gets to choose. It made Glovo its key online platform in 2023, launched its own app, Republic Dash, in 2025, and still has both aggregators on speed dial. An order through Republic Dash saves the commission it would pay Glovo or Chowdeck and keeps the customer. The aggregators bring orders it would not otherwise see. A brand with 190 kitchens and standing demand plays those options against each other. FoodCourt, with one shared kitchen and no walk-ins, has nothing to play.

Step back, and the venture-funded delivery boom is an expensive way of teaching Nigerians to want a hot meal brought to the door, and whoever owns the most kitchens in the most places, paid for by the most walk-in diners, will collect on the habit once it forms. The disruptors did the R&D, but the incumbent still owns the demand.

Cloud kitchens raise money to engineer the one thing a Chicken Republic outlet gets thrown in for free once it’s on a busy road. It might work, but so far, the assumptions aren’t as neat as first expected.

Really good read!

Looks like you had 2 versions of the rebel food section