How Nigeria Broke MoMo

No workers' day for this worker

Happy Workers’ Day and Happy Interest Alert Day from our brand partner Credit Direct!

If this newsletter was shared with you, subscribe for free:

TOGETHER WITH CREDIT DIRECT

MoMo’s promise vs hard reality

When ideas fail or companies struggle, it’s very easy to say, “Ah, I called it, always knew that wouldn’t work!” Yet some of those sentiments may not have been accurate when the product or company launched.

When MTN launched its mobile money service MoMo, for instance, the consensus was that it would crush existing fintechs and be a threat to banks. The believers weren’t crazy, although their frames of reference were mostly M-PESA or Mobile Money in Ghana.

The broad theory of MoMo’s inevitable domination was that with MTN’s subscribers and retail touchpoints, it would be easy to spread the gospel of their wallet. It had worked in other African countries; at the end of 2021, MTN Mobile Money was operational in about 15 countries, with 56.8 million customers completing 10 billion transactions worth roughly $240 billion.

In 2019, GTBank called telco-led payment services “a more compelling threat.” Nairametrics ran with the headline “Mobile money war: Telecoms threaten banks’ future in Nigeria” and argued that it would be unwise to bet against telcos.

By the time MTN and Airtel received approval in principle for mobile money in 2021, TechCabal argued that telcos were even better positioned than banks and fintechs to deepen mobile money penetration given their subscriber base, infrastructure, and agent networks.

MoMo Payment Service Bank (PSB) launched with a promise that customers could dial *671# on any network to open a wallet and send money to any phone number in Nigeria. It also started with more than 166,000 active agents and promised to reach unbanked and underserved Nigerians. Four years on, that promise is far from fulfilled.

This week, Techpoint reported that MTN Group plans to acquire a 60% stake in MoMo Payment Service Bank and Y’ello Digital Financial Services for a combined ₦95.5 billion. “It’s not just a sale; it’s a restructuring designed to shift control of these fintech units up to the group level while easing pressure on MTN Nigeria’s books,” Techpoint wrote.

The transaction will bring a ₦152.06 billion cash injection into the fintech subsidiaries while valuing them at ₦95.5 billion, more than twice their December 2025 carrying value. MTN Nigeria is moving more of the fintech risk, funding, and upside to MTN Group, while keeping a minority stake in case those subsidiaries improve.

A few weeks ago, we looked at MTN Nigeria’s FY 2025 numbers and saw MTN had written down the value of its fintech subsidiaries by ₦62.56 billion. MoMo had 3.7 million active wallets at the end of 2025, miles from its 30 million to 40 million target. The company had discussed “Fintech Structural Separation” and “Fintech Capital Injection” and even held an ad hoc committee meeting on “Fintech Strategy.”

As I wrote then, those were not “the agenda items of a business gliding elegantly toward destiny.”

Whatever happened with MoMo, given that its destiny seemed to be that of an inevitable segment winner?

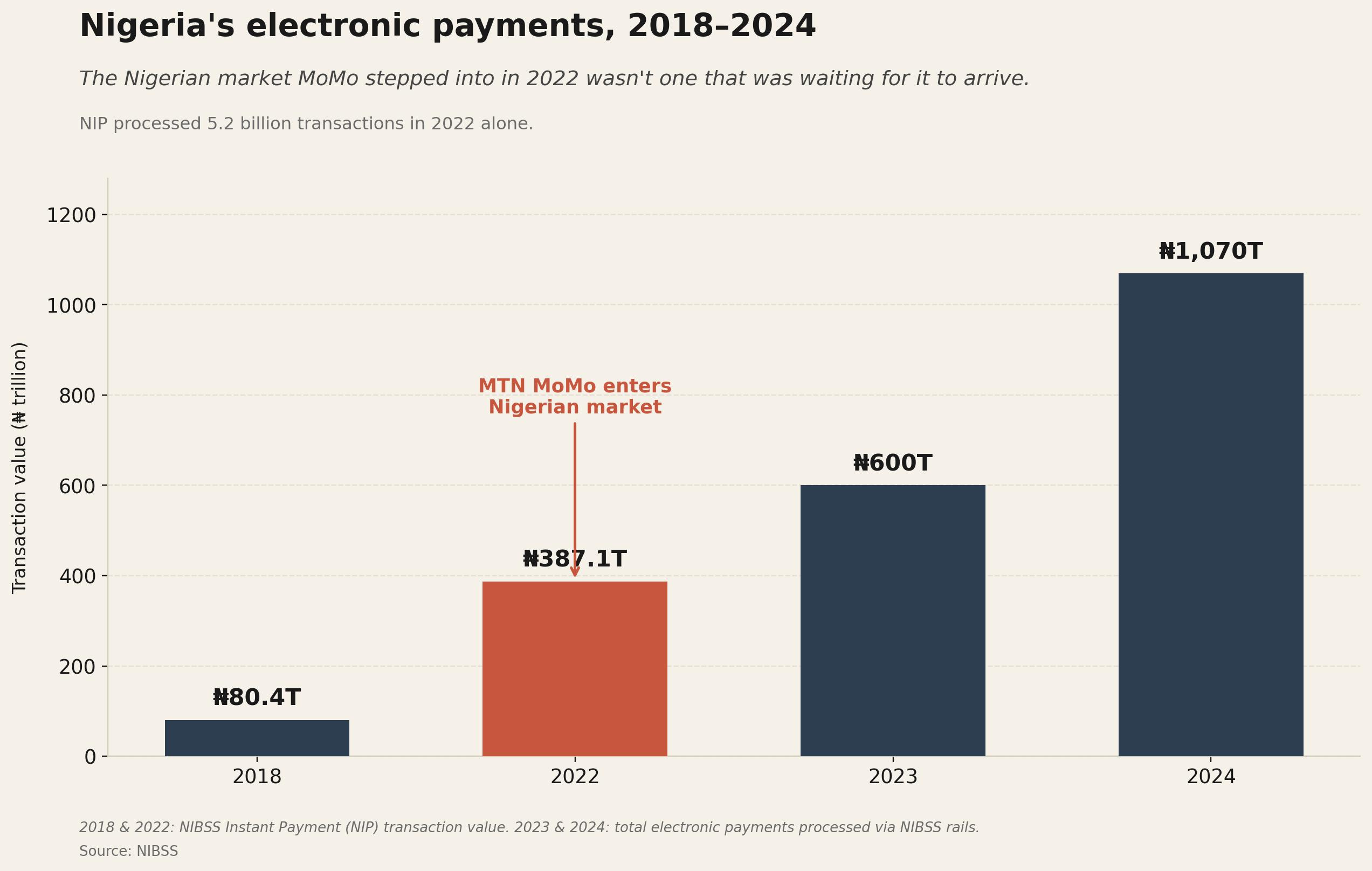

The problem starts with the market MoMo entered. Instant payments in Nigeria were already normal, and NIBSS Instant Payment transactions had reached 5.2 billion in 2022.

In some markets, the telco wallet became the main rail. In Nigeria, NIBSS, banks, POS agents, and fintech wallets had already done much of that work. So MoMo was entering a market where money movement was commoditised, so what was its edge going to be?

It was certainly not the price. MoMo’s flat ₦10 transfer fee was only competitive for amounts above ₦5,000, meaning it was not enough to change behaviour in a market where many everyday payments were small, frequent, and already moving through bank apps, POS agents, OPay and PalmPay.

A payments product needs a wedge. It must make money movement radically easier, be accepted in more places, be trusted more than alternatives, be cheaper or more reliable, give users a second product they badly want, or own a high-frequency habit before asking people to change financial behaviour.

MTN employs a lot of smart people who understand the constraints. In 2023, Eli Hini, then MoMo PSB CEO, explained the fintech’s strategy as using MTN’s “wide distribution network” and the mobile phone as the key channel, whether a basic feature phone or smartphone. In another interview, he suggested that the idea was to take money from under people’s pillows and beds and bring it into the financial ecosystem, a.k.a financial inclusion.

Compare that to what the fintechs it was supposed to dominate were doing.

OPay and PalmPay focused on being physically present when banks failed and ATMs ran out of cash. During the 2023 cash crunch, Semafor reported that vendors and customers turned to OPay and PalmPay because traditional banks could not handle the surge in online transactions. By March 24, 2023, both apps were ranked first and second among Nigeria’s most downloaded finance apps on Google Play.

In hindsight, there was still a huge cash-to-digital opportunity in Nigeria, but the fight was about who could make a market woman, student, dispatch rider, and salary earner trust that the wallet/product would work right now.

OPay answered that question with free transfers, ridiculous subsidies, agents, aggressive customer support, a consumer app that felt lighter than most bank apps, and the good fortune of a cash crunch that made everyone reconsider their banking habits. PalmPay was bundled on Transsion phones even before you made a payment choice.

Moniepoint focused on merchants and in-person payments, then expanded from the business owner to the customer. It now claims to process more than 800 million transactions monthly, with over $17 billion in monthly value, and that two out of three adults in Nigeria make payments through a Moniepoint terminal.

MoMo’s MTN Problem

A telco is excellent at reach, billing, SIM registration, airtime, USSD, and regulatory negotiation. But consumer finance is not only reach; it is product obsession, fraud control, merchant acceptance, customer service, pricing discipline, incentives, dispute resolution, and thousands of tiny moments where users decide whether to keep trusting you.

Then there is the Payment Service Bank licence that can accept deposits, hold wallets, provide payments, issue cards, run agents, and offer remittances. But it cannot lend or accept foreign currency deposits.

That matters because payments alone is a marginal business. Payments will attract users, but credit, merchant tools, working capital, savings yield, and commerce deepen the relationship.

A wallet that only moves money is useful, but in Nigeria, money already moves, so your wallet must either be more reliable than the banks, more present than cash, more rewarding than alternatives, or attached to another product people urgently want.

Again, MTN has smart people, and they also know this. Its executives talked about financial education, mobile device financing, SME exposure, online payments, remittances, and collaboration with banks and fintechs.

“Agents determine the fees they want to charge, so fees are not constant or controlled. That also doesn’t help customer adoption.” - Eli Hini (2023)

Again, what is MoMo’s sharp wedge? If it’s rural inclusion, why does it look like many PSBs are focusing on cities and competing for already-banked customers?

If it is agents, then why has the agent network shrunk dramatically?

If it were merchants, why have OPay, PalmPay, Moniepoint, and the banks become the names people associate with everyday payments?

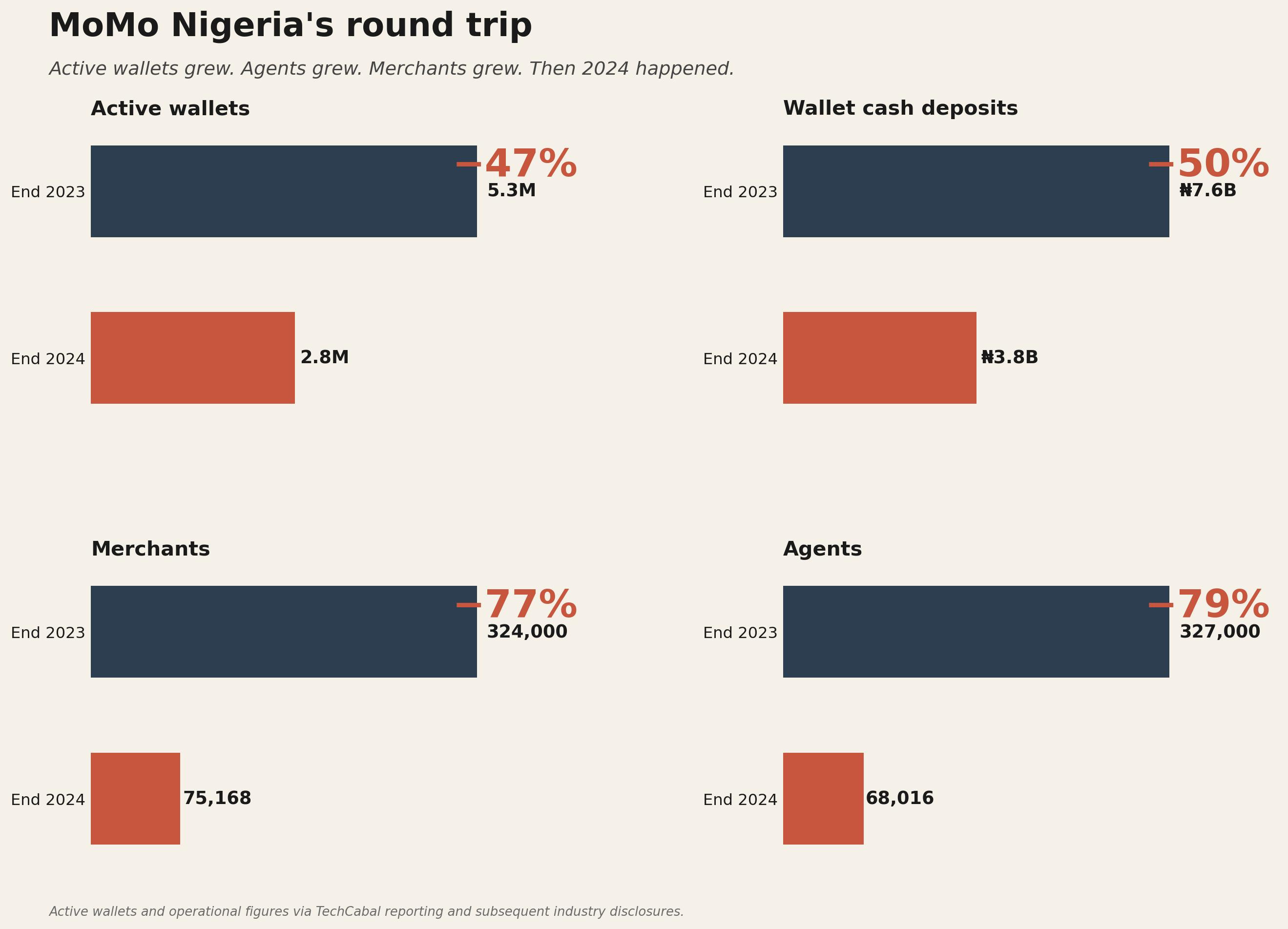

MoMo had 3.5 million active wallets by Q1 2023, according to Hini. By the end of 2023, TechCabal reported that active wallets had risen to 5.3 million, supported by an agent network that had grown from 103,000 to 327,000 and a merchant ecosystem that had reached 324,000 merchants. By 2024, those numbers declined.

MTN’s interpretation was that it was improving the quality of the ecosystem, and that is possible. Not all wallets are equal, and not all agents are useful; some customers exist only because of incentives, and some agents transact only because commissions exist, so cleaning that up can make the business healthier.

But when a fintech business loses that much surface area in a market where competitors are becoming more visible, they have to prove that what remains is a smaller, better machine.

We can’t talk about MoMo without that security incident that cost the company roughly ₦10 billion. Hini called it a technical glitch, said no customers lost money, and that MoMo had reviewed protocols and improved controls around integrations and partnerships. For a payments business trying to build trust in its first year, a major loss involving integrations impacts product confidence.

MoMo came with a distribution thesis into a market where distribution had already become a knife fight. It expected its reach to do more of the work than it could with a constrained licence in a market where the most valuable fintech loops required either lending, merchant economics, stronger consumer incentives, or brutal last-mile execution. It launched into a Nigeria where instant payments were already massive, bank transfers were already normal, and the remaining prize was not “teach Nigerians that digital money exists.” The prize was “be the financial product they trust when cash fails, banks break, and every failed transfer has immediate consequences.”

OPay and PalmPay met that moment from the consumer side. Moniepoint met it from the merchant side. The banks, for all their failures, still held salaries, corporate accounts, cards, credit relationships, and decades of customer inertia. MoMo had MTN’s brand and distribution, but it was never really clear why a Nigerian who already had a bank app, OPay, PalmPay, a POS agent nearby, and a Moniepoint terminal in front of them needed MoMo as their primary wallet.

Anyway, as it stands, MTN Nigeria has a telecom business to protect, especially after a brutal 2024 and a much better 2025. Moving MoMo and Y’ello Digital into a better-capitalised HoldCo could reduce pressure on MTN Nigeria’s books, bring fintech expertise closer to the asset, and create room for partnerships or future regulatory changes. MTN Group has the broader fintech ambition, the continental playbook, and more reasons to keep funding the experiment.

Yet a separate MoMo still has to answer the same old question. What does it do that Nigerians do not already get from OPay, PalmPay, Moniepoint, their bank, or the POS agent beside their street?

P:S: Will OPay IPO before the Butterfly Fintech? We’ll talk about it only on Sunday.

See you on Sunday!

You'll have to start paying for using my lines

The fintech space seems tough in Nigeria and the players are dominant.

There’s a lot of smart people within MTN, I’ll give it time and see how they make this work in Nigeria