A supply-side reckoning

Where goes food delivery from here?

If you missed last week’s Notadeepdive, catch up here and here. If this email was forwarded to you, subscribe here for free:

TOGETHER WITH CREDIT DIRECT

Spend it or grow it. Most people choose without realising they’re choosing.

Yield by Credit Direct grows your money at up to 21% per annum. The decision is yours. Make it the right one.

A supply-side problem

In America, roughly 400,000 independent restaurants compete for visibility, which makes an aggregator useful. The same oversupply is why the platforms can charge high commissions; with no single restaurant being indispensable, food delivery platforms take 15 to 30% on each order, on restaurant margins of 3 to 5%.

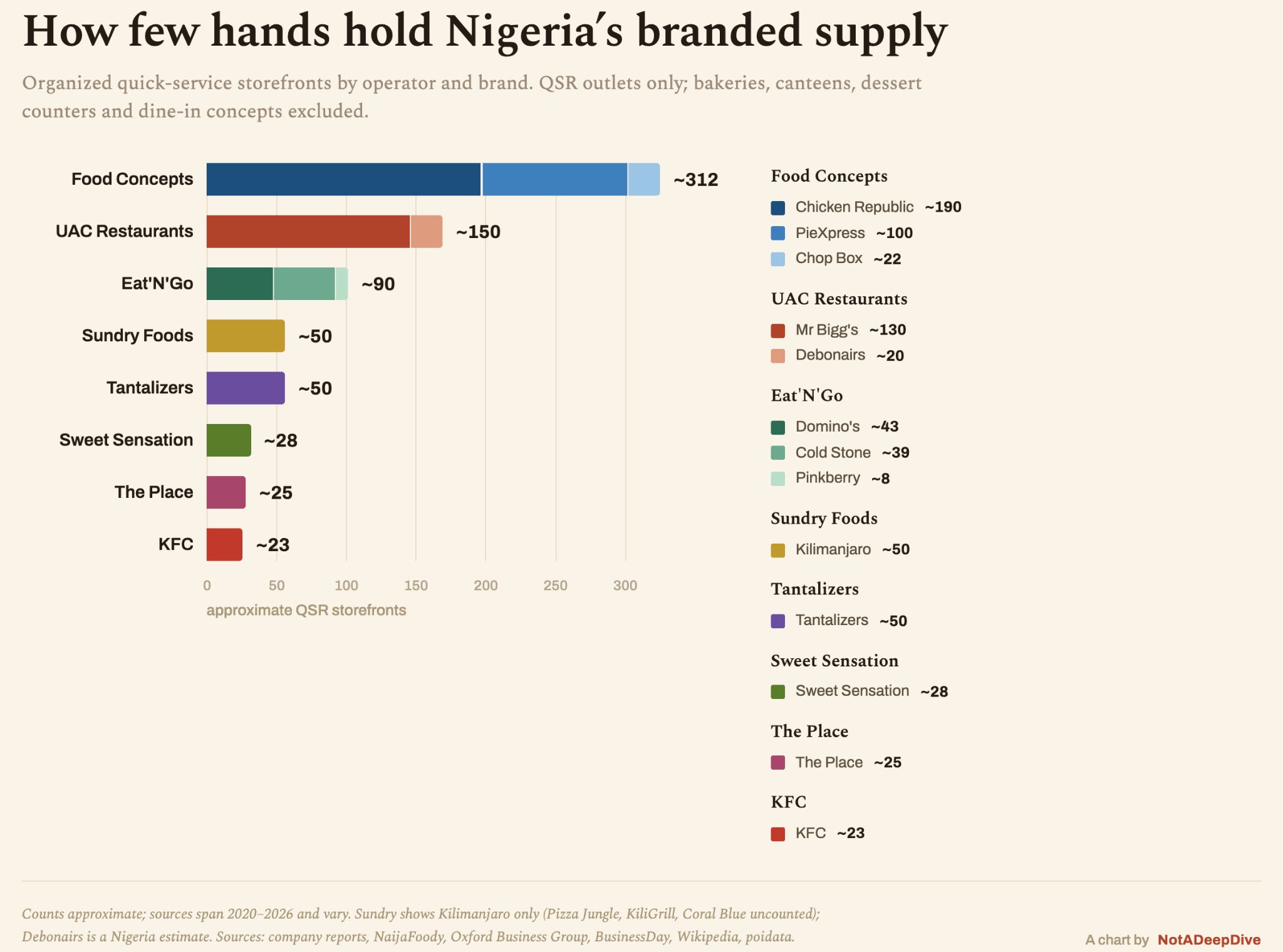

In Nigeria, bukkas and independent kitchens feed most of the country. Only four Quick Service Restaurant franchises have more than thirty outlets each, and below them, a few large single-brand chains.

The restaurants that can supply delivery platforms at scale have the kitchens, footprint, and discipline to produce at volume. What they lack—software, last-mile logistics—they can buy. Yet, for now, the specialisation of restaurants and delivery platforms suits everyone. The restaurants get demand they didn’t generate, and the platforms get users and retention. If the dynamics broke tomorrow, major restaurant chains would lose a sales channel, and the platform may lose its reason to exist.

In changing the balance, a restaurant may decide to go directly to the customer; after all, software has never been cheaper. The hard (and valuable) half is the messy business of logistics. All that to say: Chicken Republic is pushing its own delivery app (again!) while continuing a partnership with Glovo and Chowdeck.

Chicken Republic

Chicken Republic has been one of the food delivery apps’ biggest suppliers for years, Chowdeck named it one of its fastest-growing partners in 2025. For most of that stretch, the channel was close to being invisible on Food Concepts (Chicken Republic’s parent company)books until 2025. The trade receivables the company booked from its online partners over the year, i.e, Glovo and Chowdeck, grew from under ₦800 million to ₦12.6 billion.

In August 2024, Food Concepts signed an exclusive delivery deal with Chowdeck in Lagos and Ibadan, pulling the chain off rivals like Glovo and HeyFood in those cities. This came a year after Chowdeck onboarded the chain and saw a surge in its order volume. By one analyst’s estimate, Chicken Republic may account for thirty percent of Nigeria’s food-delivery order volume, with multi-brand restaurant chains completing the pie.

It may be one reason Food Concepts launched Republic Dash, a first-party ordering app carrying Chicken Republic, PieXpress, and Chopbox, the three brands under its roof in 2025. (Was the name inspired by DoorDash?)

Republic Dash is in select cities across Nigeria and Ghana, and it has crossed ten thousand installs on the Play Store. It has a companion driver app, though it is still unclear if Chicken Republic hires riders or uses another company’s fleet.

In its 2025 report, Food Concepts describes Republic Dash as a way of “building direct relationships with our most valuable customers.” It filed the app under omnichannel alongside its current delivery partners.

Chicken Republic began taking website orders as early as 2015 and ran phone-and-web experiments through the pandemic. All of it amounted to nothing, so it is easy to file Republic Dash alongside those forgotten experiments.

But the earlier attempts failed due to timing. The market education that makes a direct channel viable and the slow work of educating customers did not exist until recently. The platforms that invested in customer education are now gone: OFood, Jumia Food, Bolt Food.

Also, building a proprietary stack historically meant expensive custom software and idle courier fleets. But cheap engineering is now abundant, last-mile logistics has become something an asset-heavy chain can buy, and the sales numbers suggest there’s something to fight for.

And Food Concepts is not the company it was years ago, and neither is the food delivery market it operates in a semblance of its former self. The restaurant chains have taken a long, unpaid education in the economics of selling food online, courtesy of the very apps it fed. What it brings now is a central kitchen, distribution fleet, centralised procurement, warehousing and dedicated production units. It is the infrastructure that makes the chain indispensable to the aggregators, and the same infrastructure that app-native food delivery apps with their in-house kitchens, like FoodCourt, have been trying to assemble.

The Illusion of Dominance?

The truly scarce input in Nigerian food delivery is standardized, branded, delivery-ready food. Very few kitchens can produce a consistent product at scale under a trusted brand name.

When supply is this thin, durable value accrues to the producer, not the courier. Aggregators look dominant because they currently control demand generation and last-mile fulfilment. To fill out their catalogues, they have onboarded informal vendors diligently. But the chains drive the volume. When Jumia Food launched as HelloFood in 2012, and when later aggregators entered, their growth engines were the same institutional names. Those brands were part of why users downloaded the apps in the first place.

The platforms have rarely turned that volume into success. Jumia Food lost money for a decade before shutting down its continental footprint in late 2023. Bolt Food had exited Nigeria weeks earlier, reportedly having lost primary quick-service franchises to competitors. The platforms absorb the heavy capital losses of the logistics layer, while the franchises keep the customer and outlive the tech companies built to serve them.

Part of what makes the chains defensible is economies of scale. Buying ingredients by the metric ton lets the chains absorb currency shocks and pass some of the savings to the consumer. A nascent food delivery operator juggling delivery and its own kitchen operations buys raw inputs closer to retail prices.

The squeeze runs down into the courier network. Aggregators are caught in a multi-sided bind: they cannot raise delivery fees on a price-sensitive consumer, and they cannot cut rider payouts without losing riders to competitors.

Can the Chicken go the last mile?

Yet the fast-food business is also a struggle. Even Nigeria’s best-run QSR groups keep less than seven naira of every hundred they generate. Food Concepts recorded a net profit margin of 6.7% in 2025, up from 3.5% the previous year. This thinness leaves little to fund an expensive tech operation.

Cloud kitchens, food delivery apps that produce their own food, across the world have demonstrated that cooking and packing food, maintaining logistics operations, generating demand and managing customer-relationship software are distinct and capital-intensive businesses.

Being cost-efficient and successful at one says nothing about the other three.

Chicken Republic’s decade of failed logistics experiments may also suggest a structural inability to manage delivery. Republic Dash has 10,000 downloads; Chowdeck claims over 1.5 million users and says it is profitable.

There is little evidence that a legacy fast-food operator has the institutional muscle to pull off this adventure. If Republic Dash tries to compete as a discovery engine for its own brands, it may struggle to outspend platforms for the digital attention it used to receive for a small commission.

But there is a narrower, more plausible version of the bet. City-wide rider availability is essential for a marketplace connecting thousands of restaurants to millions of homes. But a single chain delivering its own food from local outlets to repeat customers within a fixed radius faces a simpler operational problem.

Aggregator Defenses

The platforms are not waiting to see how this plays out. In the past two years, they have been spending to get ahead of suppliers who may route around their marketplaces.

Much of the investment is going into groceries, where supply is abundant and substitutable. Grocery delivery is a category nobody loves on margin, about 1-3%, and everybody wants on frequency. Glovo is running micro-fulfilment dark stores in select locations. Delivery Hero, its parent company, has found that customers who order food and groceries spend more than five times what food-only customers do. Chowdeck is reportedly opening two dark stores weekly, aiming for five hundred by the end of 2026, stocked through an exclusive partnership with the bulk e-commerce platform GoLemon, which handles sourcing and quality control while Chowdeck runs fulfillment.

Another sharp move is to get inside the merchant so that leaving the platform costs something. Last June, Chowdeck bought Mira, a point-of-sale system for restaurants. This backend integration has the potential to create an operational dependency that discourages vendors from switching from the platform, and even if they do, convert them to customers of a different product within its ecosystem.

Glovo is chasing the same supplier lock-in with loans. Through a 2025 partnership with the fintech Salad Africa, Glovo extends working-capital loans to its restaurants, underwritten by their real-time sales on the app and repaid as a slice of future orders processed through Glovo. A restaurant carrying the platform’s working capital may find leaving complicated.

Chowdeck built Relay, an on-demand, white-label logistics utility, reachable by API or dashboard and paid strictly per drop. If a chain like Chicken Republic migrates customers to a first-party app to escape marketplace commissions, Food delivery apps can still earn on the volume by serving as the underlying courier, without carrying the cost of acquiring those customers. By selling last-mile to the vendors expanding beyond its app, the biggest supplier can become a customer of a different product.

Both major platforms are building defenses around the concentration risk of depending on a few corporate kitchens. Read together, Chicken Republic’s app and the aggregators’ countermoves are the same strategy executed from opposite ends of the value chain. The supplier is integrating forward into delivery; the aggregator is integrating backward into supply.

If platforms keep their margins by owning discovery and the grocery run, while the chains find that going direct costs more per order than the commission they already pay, concentration is a feature the market can live with, and Republic Dash will remain a marketing curiosity.

See you on Sunday!

| A guest post by

|

Hey Mother

Very insightful